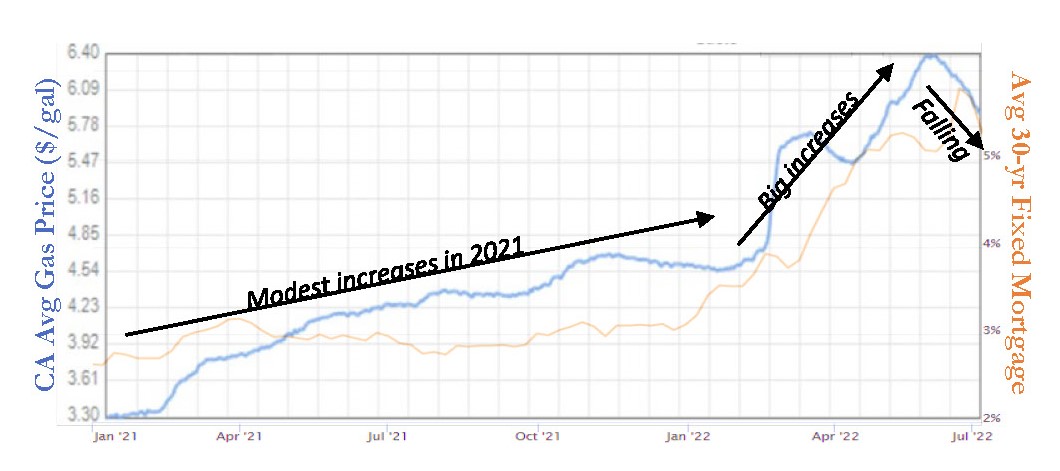

Pump prices & mortgage rates have been in lockstep together, and both are headed down!

A client recently asked me where he could go to see current mortgage rates. While there are more sophisticated research tools, I told him the easiest place to gauge rates at the moment is at the gas station!

We see gas prices every day driving around town, wincing as we fill up, and giving real-life math questions to our kids in the car (or am I the only person that does that last one??!!). You may not remember how much you paid for your last gallon of milk or your last loaf of bread you purchased, but I bet you recall the price of your last tank of gas ($105 for me; OUCH!).

Conveniently, mortgage rates have been in lockstep with California gas prices. This makes following mortgage rate trends as easy as peeking at the gas prices as you drive by. Check out the graph & numbers below to see for yourself.

| | CA Gas Price per Gallon | 30-yr Fixed Mortgage Rate |

| Increase since Jan 2021 | $2.67 | 2.95% |

| Peak (amount) | $6.44 | 6.28% |

| Peak (date) | 6/14/22 | 06/14/22 |

| Current (7/13/22) | $5.65* | 5.72% |

*Price paid for regular unleaded at Arco on Folsom Blvd

Oddly, the price for gas (in $) has been & is nearly the same as a 30-yr mortgage rate (in %)! While its impossible to predict what these prices and rates will do in the future, the recent correlation between gas prices and 30-yr mortgage rates is unmistakable. Even if you drive an electric vehicle or own your home debt-free, its important to keep tabs on gas prices and mortgage rates. They are the bellwether for so many other pieces of our economy.

So the next time you’re casually curious if mortgage rates are rising or falling, just look at the pump! Both are currently in the largest decreasing trend since the early days of the pandemic. Lets hope they both continue to drop!