You probably noticed recent news articles that went something like this…

“For the first time in 3 years, The Fed raises interest rates!!!”

This headline gets overly-simplified and makes the reader believe that ALL interest rates, including mortgage rates, increased overnight because of the government. That is simply not true. In fact, mortgage rates LOWERED slightly immediately after The Fed’s recent rate rise announcement. Let me paint a more accurate picture.

The Federal Reserve Board (aka- The Fed) has direct control over a single rate, The Federal Funds Rate. Some types of loans are indeed coupled to this rate, so The Fed’s decisions have a direct impact on these loans. But fixed rate mortgages ARE NOT one of these types of loans. Mortgage rates move not based on government decisions, but rather by open-market supply & demand.

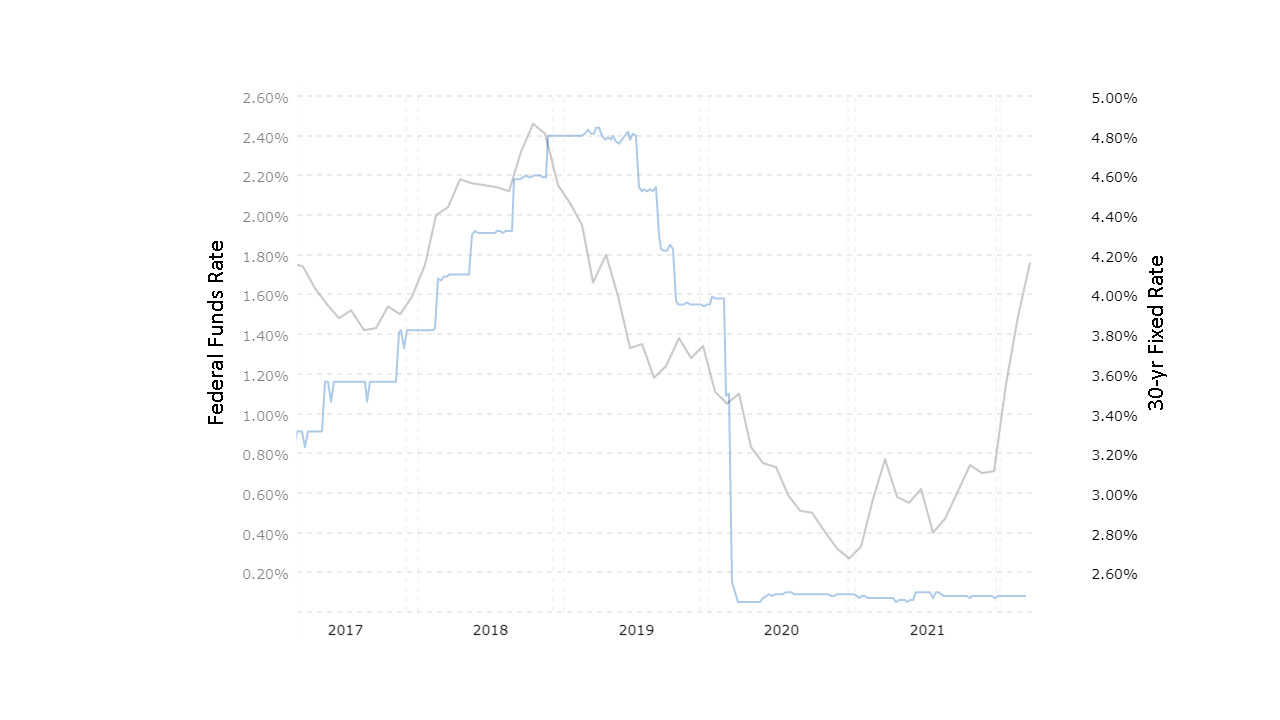

Below is a graph that shows both the Federal Funds rate (the blue line) and 30-yr fixed rate (the gray line) over the last 5 years. You can see there is no direct correlation. Surely, in 2019 they both were generally declining, but not at the same time nor pace.

As in most things, open market dynamics force changes more quickly than bureaucratic decisions. The chart shows the gray line’s peaks and valleys all pre-date the blue’s, with the exception of The Fed’s decision to plummet the Federal Funds Rate to nearly 0% at the onset of the Covid-19 pandemic. With the Fed’s rate finally rising, it doesn’t necessarily mean mortgage rates will continue to rise along with it. Perhaps mortgage rates have already hit their peak??

Here’s the takeaway…last week’s headlines of rising rates are old news for mortgages, and don’t ever assume that mortgage rates will change due to a Fed rate change. Actually, mortgage rates have slightly improved since The Fed’s recent rate increase!

30-yr rates are now over 4%, so where do they go from here? Much of that answer depends on the war in Ukraine, the cost of gas at the pump, and evolving expectations of this year’s mid-term elections. Good luck correctly predicting the outcome of those story lines!!!

But, I will leave you with one more graph to consider as potentially a glimpse into the future. Below is an illustration that shows the difference in interest rates from long-term to short-term US government bonds. When the short-term bond has a higher rate than a long-term bond (a very unlikely event), the line’s chart goes into the pink negative territory. Economists call that an “inverted yield curve,” and this financial anomaly has taken place before every US economic recession over the last 60 years.

Presently, the difference from long to short term bond rates precariously sits at only +.2%, and has been falling in recent weeks. If this figure indeed becomes negative and an inverted yield curve is realized, it could foreshadow an economy headed for a recession. Mortgage rates nearly always fall during recessions, so its conceivable we will see lower mortgage rates in the near future. Stay tuned, and thanks as always for reading!