Expect more sales, lower rates, and bottoming home values

2022 was a rough year for the real estate market. Interest rates and home values both changed course at the fastest pace on record, causing many potential buyers & sellers to hit the pause button on their transaction efforts. As we enter a new year, sellers likely have been waiting for the rain to finally end to list their homes, while buyers have been waiting for lower rates and home values before jumping back in the market. Will the current “bear” real estate market end? Will a “bull” market return? Read more as I share my insight on what’s ahead for our market (& read all the way to the end for why they are called bear & bull markets!)

The bear market will come out of hibernation (but don’t expect a bull market to return)

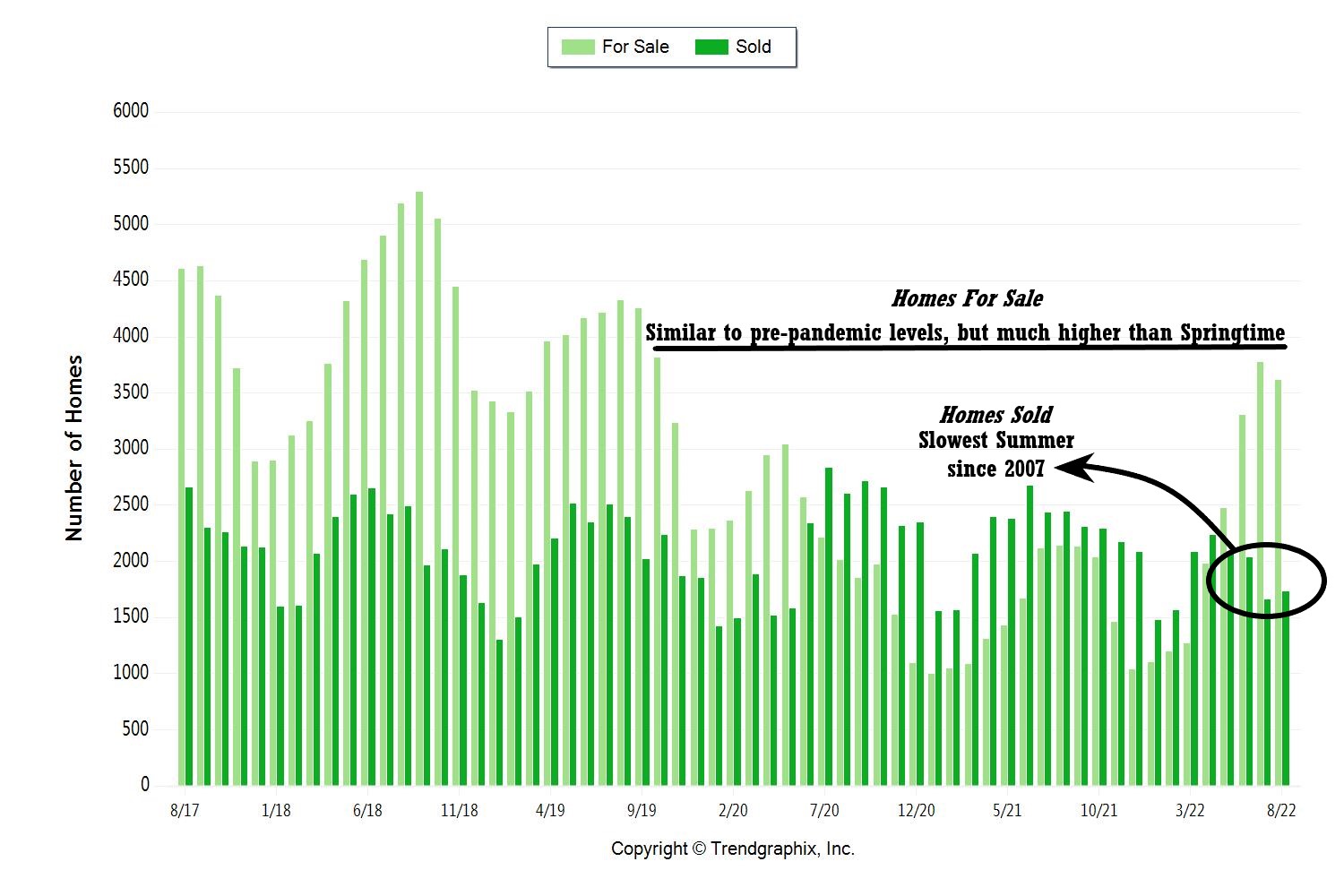

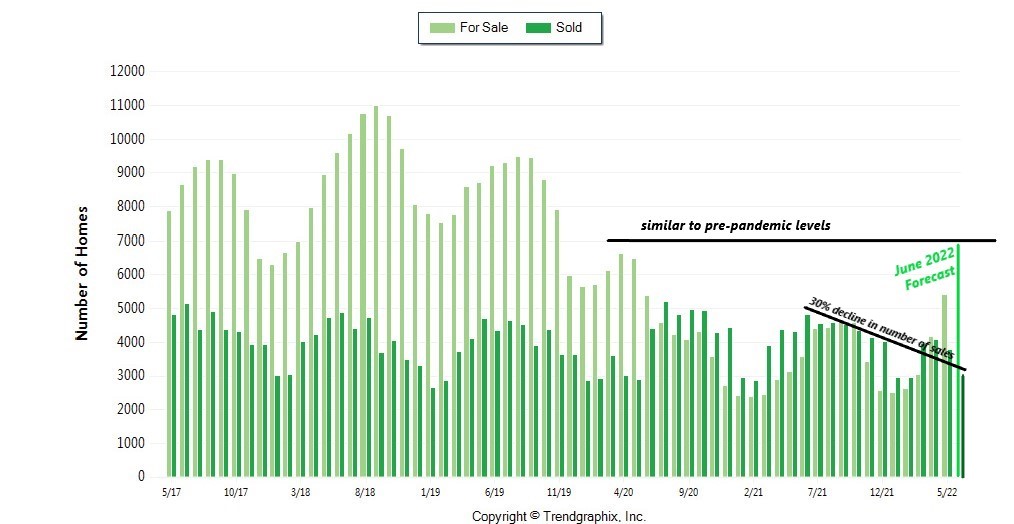

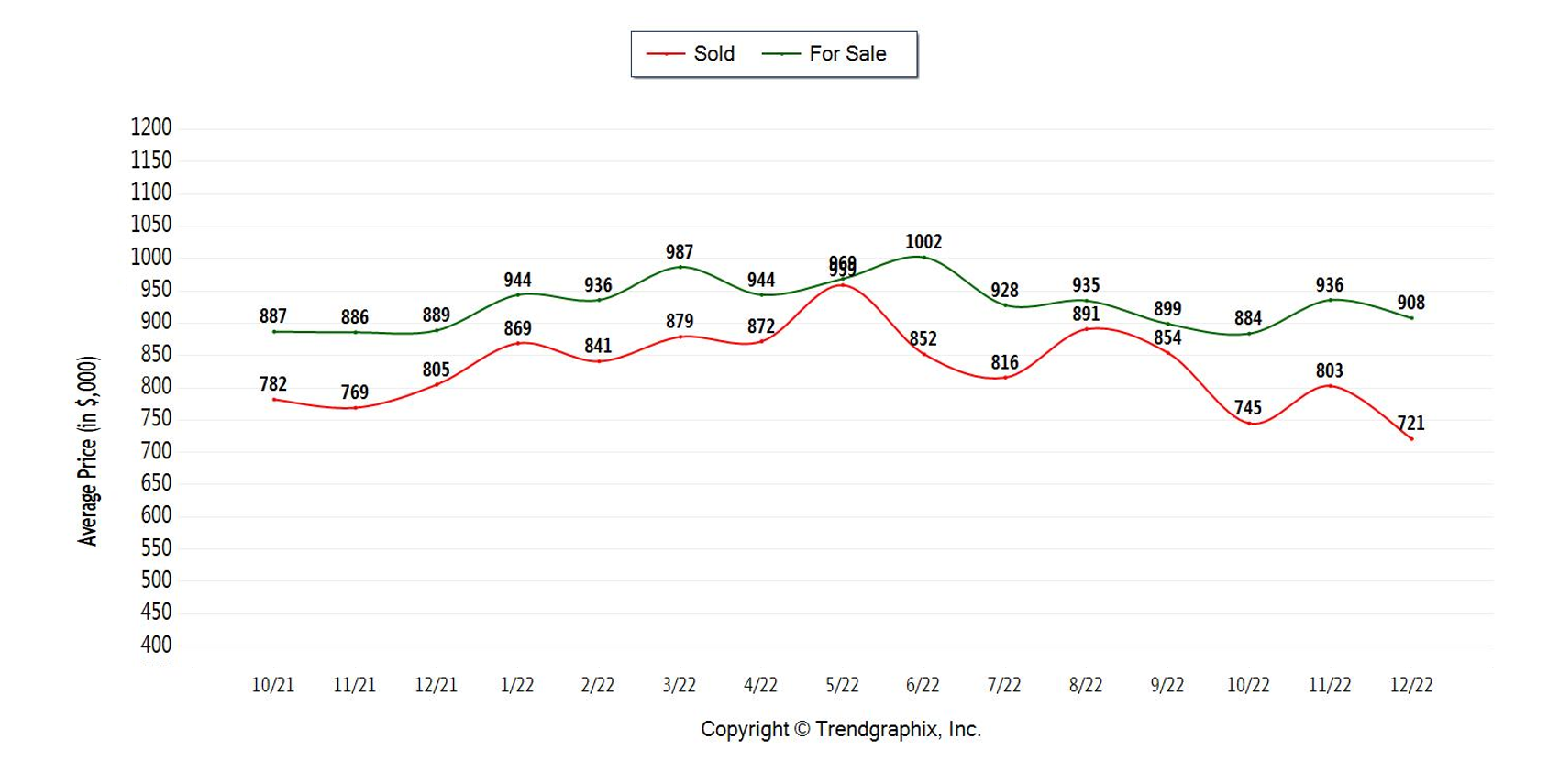

Most regions throughout California have become “bear” markets, meaning home values have fallen consistently and considerably. Take Folsom, for example, where the average home price fell 25% from May to December. That’s a sobering statistic for current home owners considering selling, but keep in mind the current values are still higher than they ever have been if you exclude the insane Covid-related boom. These recent declines are largely due to higher interest rates and hesitant home buyers, but also because of SIGNIFICANTLY fewer home sales. To be precise, the 4th quarter (October-December) was the slowest quarter in over 20 years in Sacramento County, with fewer than 30 homes selling per day in a county comprised of over 600,000 housing units!

Expect the market to pick back up in 2023 as more sellers put their homes up for sale and buyers eagerly purchase them. Affordability has improved due to declining home values, thus inspiring first-time home buyers to get back into the market. After 3+ years of competitive bidding wars and few homes for sale, buyers are now calling the shots in transactions. The typical listing is selling for 6% less than the asking price, with sellers often paying credits towards closing costs and home repairs. Many buyers will score great bargains on homes this year, but they shouldn’t expect rapid price appreciation to return to the market just yet.

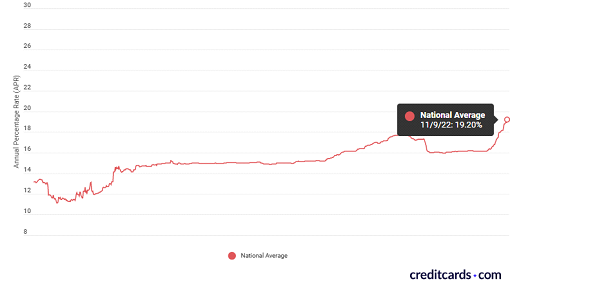

Interest rates will settle down (but don’t expect record lows to return)

Interest rate declines are also helping affordability. Yes, you read that right…interest rates are going down! After peaking at nearly 7.5% in October, 30-yr fixed rates are settling down near 6% in recent days, and likely poised to drop further in the months ahead (more on that in a future post).

While rates aren’t likely to plummet back to 3%, 30-yr rates in the ~5% range will help to stabilize the real estate market and reduce the sting buyers feel when calculating their monthly payments.

Sacramento home values will bottom out (but don’t expect big price gains to return)

The worst is likely behind us with falling home prices. After dropping 2-3% per month since May, Sacramento area home values should find a bottom sometime this year. Rent rates remain high everywhere (1-bedroom apartments are renting for over $2,000/month!), which will help prop up home values as tenants weigh the options between renting and buying. 2023 buyers may risk some short-term losses in equity, but that is a small risk to take for the big rewards of purchasing a home in this strong buyer’s market. After 6 months of price drops, the average listing is on the market for 6 weeks & selling for 6% off the asking price. These 6s may be a troubling sign for sellers, but for buyers it’s a proverbial jackpot! Get out in the market and let me help you dictate the terms of your next home purchase!

2023 will feel like an awakening after a dormant second-half of last year. If you are a seller, you need to make worthwhile preparations to your property to make it stand out above the competition. If you are a buyer, you need to “start your engines” and follow my top 5 tips from my prior post to get ready to decisively act when the right home comes up for sale. Both sides need to be partnered with an experienced mortgage and real estate broker like me who can navigate you through this changing market. I look forward to helping more clients in the weeks ahead prepare for their 2023 transactions.

PS – Bull & Bear markets earned their names based on how these animals attack. A bull lowers its head and then surges its horns upwards in an attack, hence why a bull market is known as one that is on the upswing. Bears, however, get high and then attack down with their giant paws. When a financial market (like today’s real estate market) is going down in value, its known as a bear market. Now you know!