I recently went up to Donner Lake for a beautiful fall weekend. When I came back it felt like I brought the cool air back with me. The autumn air here in Sacramento feels crisp, healthy, refreshing.

Similarly, the real estate and mortgage markets are cooling off too. THIS IS GREAT NEWS! Much like the changing weather, the current market changes are healthy and refreshing too. After months of sizzling home price increases, we’re beginning to level off. Interest rates, too, have cooled off and have fallen from their summer highs. All of this means home buyers, particularly MOVE-UP buyers, have more opportunities to find their next home at a reasonable price.

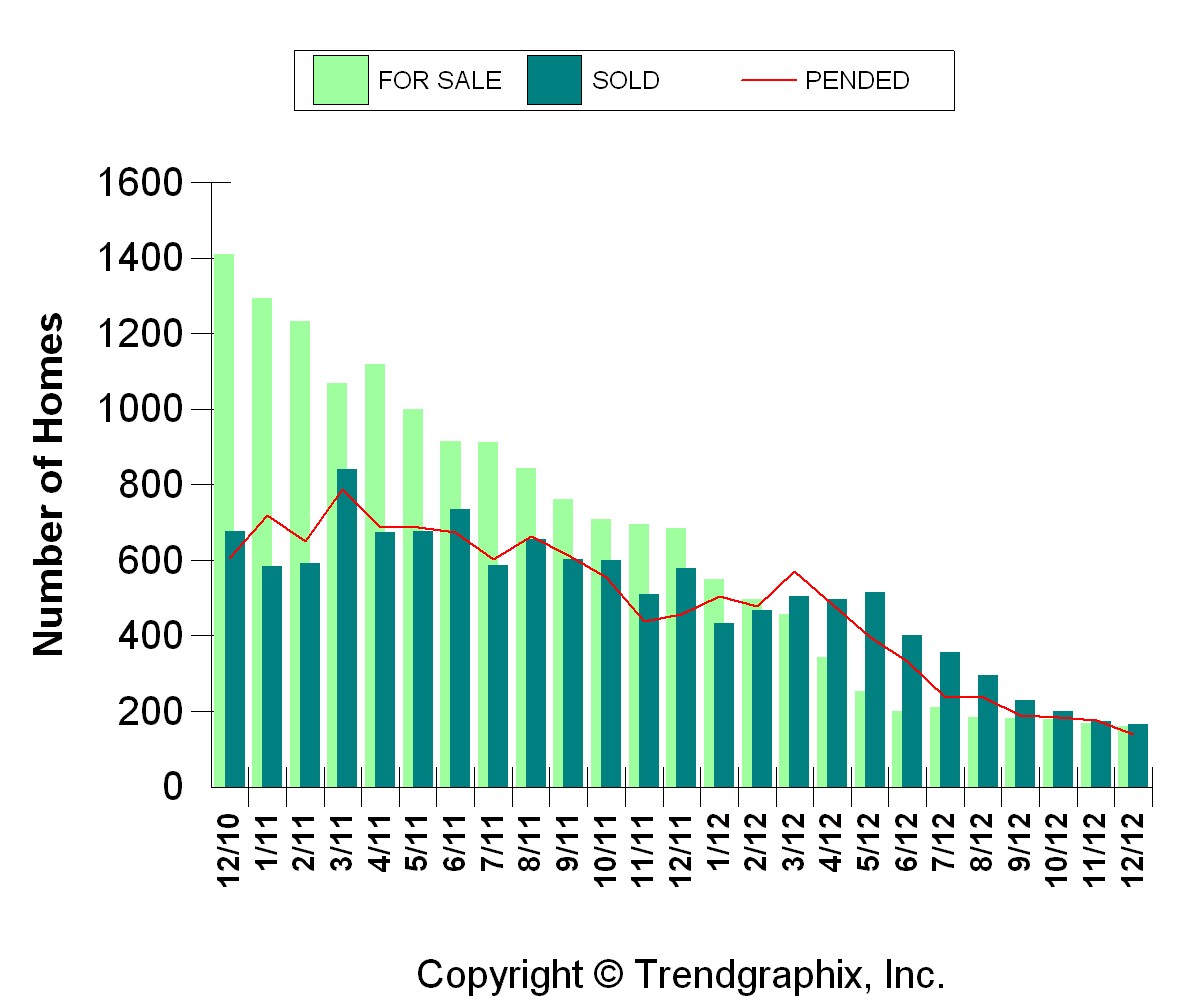

This past summer we saw an unbelievable real estate rally. Much like a caged animal, the market sprung from hibernation and jumped with reckless abandon Sacramento area average home prices spiked 13.8% from April to August!!! This rally was exciting and, thankfully, unsustainable. Had we kept on that pace, we simply would have created a market bubble that surely would have popped in the near future.

Instead, we’re seeing prices level off, homes sit longer for sale, and more homes available to purchase. This is incredibly good news for home buyers. I had several clients who looked to buy a home earlier this year who opted to sit on the sidelines and wait for the market to calm down. These clients now look very savvy & patient (you know who you are :-), as the coming months should present them a more reasonable marketplace in which to buy.

Furthermore, the interest rate spike we saw this summer is beginning to reverse. In May & June, the markets were largely expecting The Fed’s influence on mortgage rates to “taper.,” thus sending rates higher. Now, the expectation is beginning to change. With sluggish economic indicators and a political stalemate threatening to bring our country to a halt, uncertainty is high. As a result, fixed mortgage rates have fallen nearly ½% in the last month.

Again, all of this means home buyers are in a much better position to find the right home without the worry of insane, multiple-offer situations. If you are a first-time home buyer, there’s no need to panic about being “priced-out” of the market in the near-term. If you are a move-up buyer, this balanced market between buyers and sellers is the perfect environment to buy your new home and sell your old home.

As most clients know, our firm is perfectly suited to help you with all of your home buying, financing AND selling needs. Many clients find this one-stop-shop form of real estate service incredibly valuable and convenient. For the rest of the year, if you enlist us to help with all three services (buying & financing a new home as well as selling your old home), we will reduce our listing commission by ½%. On a $400,000 home that’s a $2000 discount!

Thanks as always for reading Matt’s Memos and your continued support by returning to and referring The Blue Waters Group.