Over my career, I’ve referred to my thoughts on the markets as forecasts. For example, my yearly post about the market is titled the annual market forecast, and I’ve been known to compare timing the markets with forecasting the weather.

Today I’m taking it a step further; I’m going to make a bold prediction about where interest rates are heading. I’ve never been so daring in my career, but in doing so I’m hoping to get you prepared to take advantage of what I believe will be record low mortgage rates in the coming months.

If I’m going to make such a provocative declaration, I want to back it up with data. So, as a fair warning I’m going to show you some graphs. Don’t close your browser just yet; I promise to make it impactful and easy to follow (it may be easier to watch the video starting at 1:15).

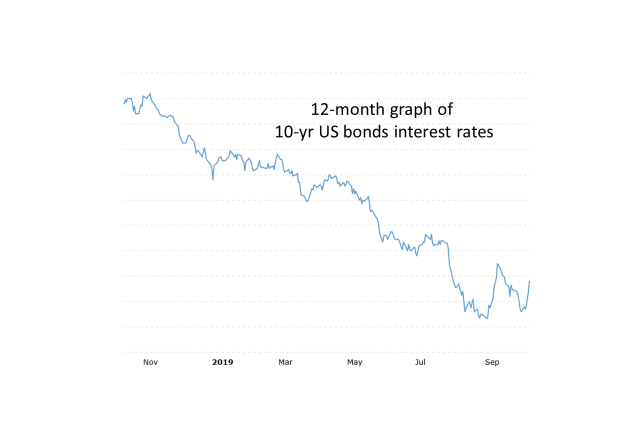

OK, here we go! Above is a graph of the interest rates on 10-yr US Treasury Bonds. These rates are closely correlated to mortgage rates, so we’re just going to focus on the direction of the rates. As you can see, rates have been in mostly a free fall for the last year, and we’ve helped many clients in the last two months take advantage of these low rates. In fact, I’d like to focus on these recent two months where this jagged saw tooth action has been and show you where on this timeline our clients have been locking rates.

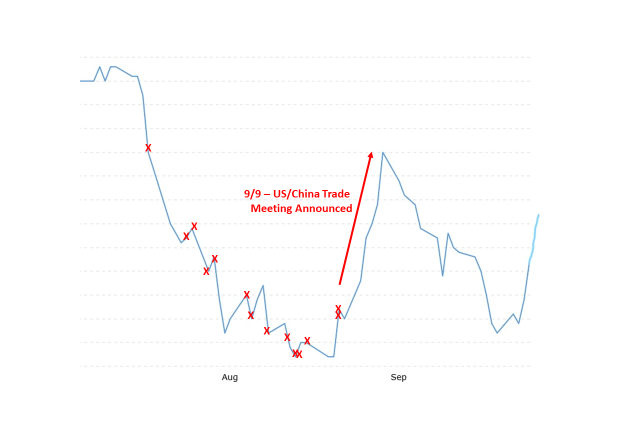

Beginning in August, refinance clients began locking in their rates; each of these X’s indicate when one of my clients locked their loan. We were on a roll until just after Labor Day, and then rates took a big jump up on the announcement of a future meeting between US & China trade officials. During this volatile time, several clients submitted an application to refinance with us, but we recommended against locking in the hopes the markets over-reacted and would settle back down. That’s indeed what occurred, and we had a number of clients lock in their low rates in the “trough”. No one locked at the peak!

Beginning in August, refinance clients began locking in their rates; each of these X’s indicate when one of my clients locked their loan. We were on a roll until just after Labor Day, and then rates took a big jump up on the announcement of a future meeting between US & China trade officials. During this volatile time, several clients submitted an application to refinance with us, but we recommended against locking in the hopes the markets over-reacted and would settle back down. That’s indeed what occurred, and we had a number of clients lock in their low rates in the “trough”. No one locked at the peak!

Now history appears poised to repeat itself. For the last week, rates have been on a steep rise as verbal agreements were made in the widely anticipated trade meetings. The US and China economies are the two largest in the world, so easing tensions of a trade war is definitely good news. But, I think the markets are being overly optimistic. First off, none of the details of this trade agreement are in writing yet. That is supposed to be done over the next several weeks. Secondly, analysts say the agreements do not address some of the more critical issues of the trade tensions; this is being called simply Phase 1 of trade discussions. And thirdly, trade and tariff policies can be set unilaterally by a president in the name of national security. They can also be changed or removed unilaterally.

Bottom line, the trade war outlook is still uncertain, and when the markets figure that out then rates will fall. There are other factors at play that support my theory, and I’m happy to share them with you individually, but for fear of losing my audience I’m just cutting to the chase…mortgage rates are poised to fall. That is my bold prediction; and here is my strong recommendation; begin a refinance application now so you can be prepared to lock in a low rate if my prediction comes true. A trusted colleague of mine put it this way…if you go tailgating at a football game you don’t want to still be in the parking lot when the big play happens. Sure, the roar of the crowd will prompt you to make your way in, but by the time you get into the stadium you’ve missed the moment. Grabbing a low rate on a refinance is much the same; you need to be in your seat, watching the game in order to participate in the exciting plays.

I can’t lock an interest rate until the needed paperwork to complete an application has been submitted. So, let’s do that now. If rates drop during the holidays do you really want to scramble to grab w2s and bank statements for me then? No, lets do it now. I’ll absorb any upfront application expenses for you, and if rates don’t drop we don’t need to complete the refi. There isn’t really any downside for you coming into the game: if my prediction is right you’ll get to celebrate with everyone on the field with a great refi rate, and if I’m wrong you’ll have a front-row seat to my crystal ball fumble.

Contact me so we can discuss ways we can make it easy for you to start your refinance application ahead of the next interest rate down turn.

March marks the beginning of Real Estate season. As snow melts and flowers bud, current and aspiring home buyers alike are coming out of financial hibernation to assess their real estate affairs. That’s why I hope this annual market forecast is a timely message to many of my clients and readers.

March marks the beginning of Real Estate season. As snow melts and flowers bud, current and aspiring home buyers alike are coming out of financial hibernation to assess their real estate affairs. That’s why I hope this annual market forecast is a timely message to many of my clients and readers.

In 95819, the median home price hit a peak of $500k in 2005.

In 95819, the median home price hit a peak of $500k in 2005.