Our team has become well-versed with the new California Dream For All Loan program and has it available to offer to our first-time home buyer clients. Lets unpack a common example and see how this program functions.

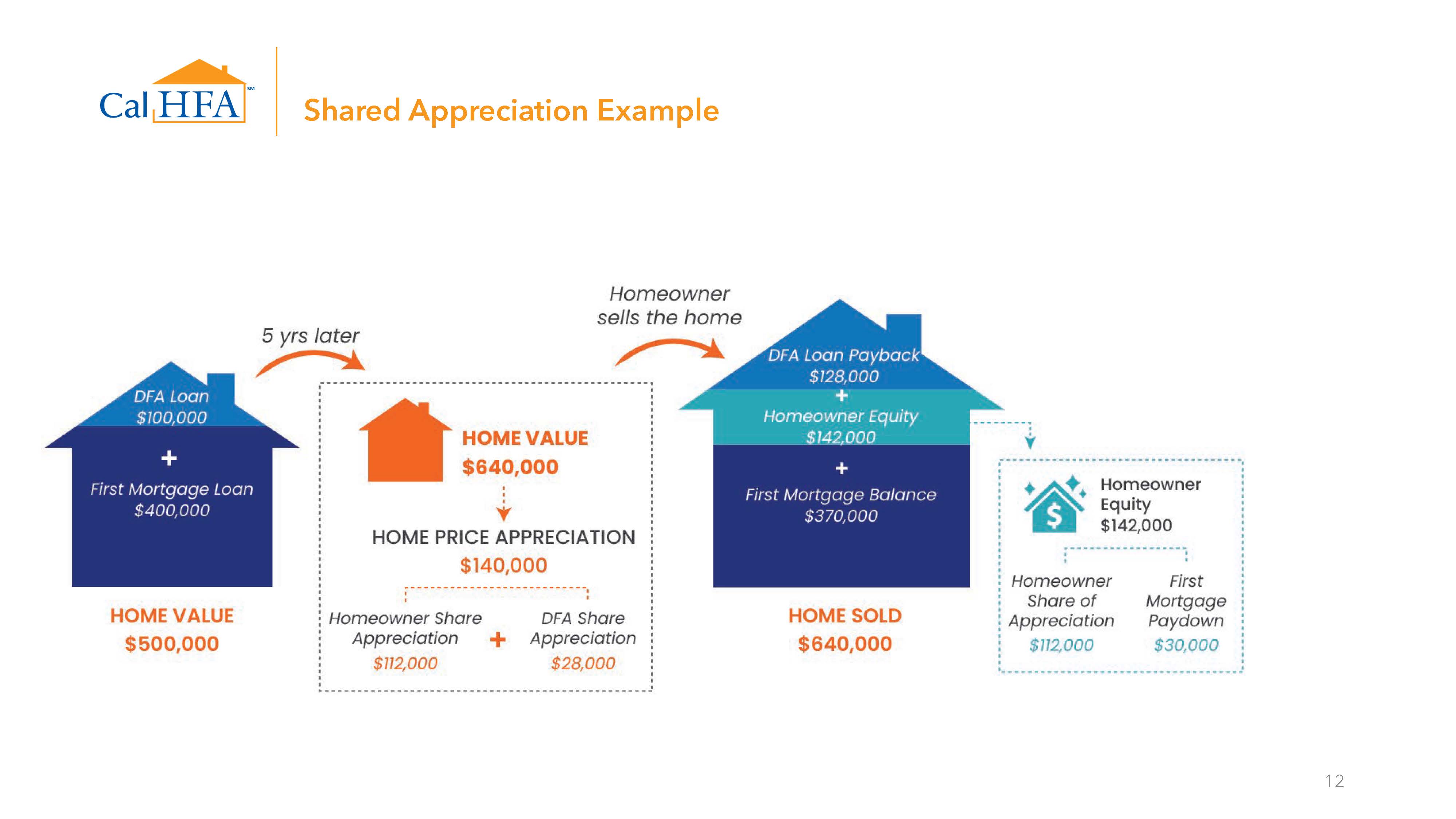

Assume someone buys a home for $500,000. They would obtain a traditional 30-year fixed loan at a fair market interest rate for 80% of the purchase price, making the loan $400,000. Now instead of making a $100,000 down payment, something most first-time home buyers don’t have, they obtain a 2nd mortgage from the state of California for the needed $100,000. No monthly payments are required and no interest accrues on this $100,000 2nd mortgage. But it is not a grant; it is not free money. This 2nd mortgage is a Shared Appreciation Loan, meaning that when the home buyer goes to sell the property they have to pay back the loan in full AND share in the gained equity with the state of California.

Lets see how those numbers work. Lets assume this $500,000 home appreciates by a modest 5% per year. After 5 years, the home is now worth $640,000; it has appreciated by $140,000. Most folks utilizing this program will need to pay back 20% of that appreciation to the state, in this case $28,000 dollars. So when they sell the home, they will pay $128K to the Dream For All mortgage, the outstanding balance of the 1st mortgage that started at $400,000, leaving them with $142,000 in equity before selling costs.

So, in a nutshell, a borrower who put in nothing for a down payment ends up earning nearly $150,000 in realized equity. And to do so, they had to pay $28,000 in shared appreciation to borrow a $100,000 loan, which essentially works out to be an annualized interest rate of 6%.

Here’s another example created by CalHFA worth watching:

Like any loan program, there are qualifying restrictions. Contact my team and I for the full details on how first-time buyers can take advantage of this new loan!

Buying, selling, or refinancing a home in today’s market can be quite an intimidating process to many. From elevated interest rates to volatile home prices, more and more elements are beyond predictability. I recently watched other real estate professionals market themselves as real estate saviors, promising the world in order to falsely take the fear out of the process for consumers (& “win the deal” for themselves). In my opinion, however, nothing is scarier in real estate than an over-promising sales person guaranteeing things they simply have no control over.

As a real estate agent and mortgage broker, I cannot be a savior. Rather, I see myself as your real estate “Sherpa.” Sherpas, as you may know, are an ethnic group in Nepal who are famous as highly skilled and capable mountaineering guides in the Himalayas. Unable to make the trek alone, summit-seeking climbers hire Sherpas to manage and navigate the dangerous trek up Mount Everest. And while Sherpas make most Everest ascents possible, the chance of reaching the summit is ultimately out of their hands.

Buying, selling, or financing a home can feel like climbing a mountain. It seems scary, danger exists if you make a wrong turn, and there are plenty of nay-sayers claiming you can’t do it. To overcome the obstacles, you need a partner who is experienced, resilient, and calm under pressure. But, be wary of the guide who guarantees you a trip to the summit; who are they to control the weather in such extreme conditions?

I cannot guarantee you the perfect house at the lowest price with the fastest close. I cannot guarantee you an underwriter will approve your loan. And I cannot guarantee your home will sell in 2 days for full asking price. There are too many variables to a transaction to pretend like I wield the real estate cosmos in my hands. Again, I am not a savior. I am, however, your real estate Sherpa, determined to use my experience, skills, and knowledge to help you make the best decisions possible during your next unpredictable real estate expedition.

The Princess Bride has been on my mind since watching it on Valentines Day (for the first time!). Lets talk real estate through one of the greatest Rom-Com story lines of all time.

Home prices everywhere have been rolling down a steep hill recently. After hitting an all-time high in May 2022 at $575,000, Sacramento’s median home price dropped over 15% by the end of the year.

But now we’re starting to see things improve. January actually had a month-over-month increase in prices, and February is seeing that trend continue.

What does this mean for the future of home prices? After experiencing a violent roll downhill, no one is ready to sprint back to the top right away. The market will likely lay idle at this level, catching its breath and finding its footing.

Later this year, it could be a treacherous journey through the real estate “fire-swamp,” as the three terrors of inflation, recession, and R.O.U.S. (Rates of Unusual Size) stand to spook possible buyers & sellers from re-entering the market.

Bottom line…finding bottom is very different from being in recovery. I’ll keep you updated as the market heats up approaching the spring buying season.

This 6-6-6 sign is indeed a great omen for buyers!

Back in September, I explained in a video post the troubles ahead for our market as 30-yr mortgage rates hit 7% for the first time in 20 years. Homes were becoming increasingly unaffordable as high rates and home values squeezed many would-be buyers out of the market.

Thankfully, some balance has been restored as both rates and values have receded, meaning there is now hope ahead for the market. Today I want to walk you through some points to see how today’s affordability is back in line with historical norms, and why if you are a buyer you should be getting excited for a home purchase in the year ahead. Either click on the video above or read below for the full insight.

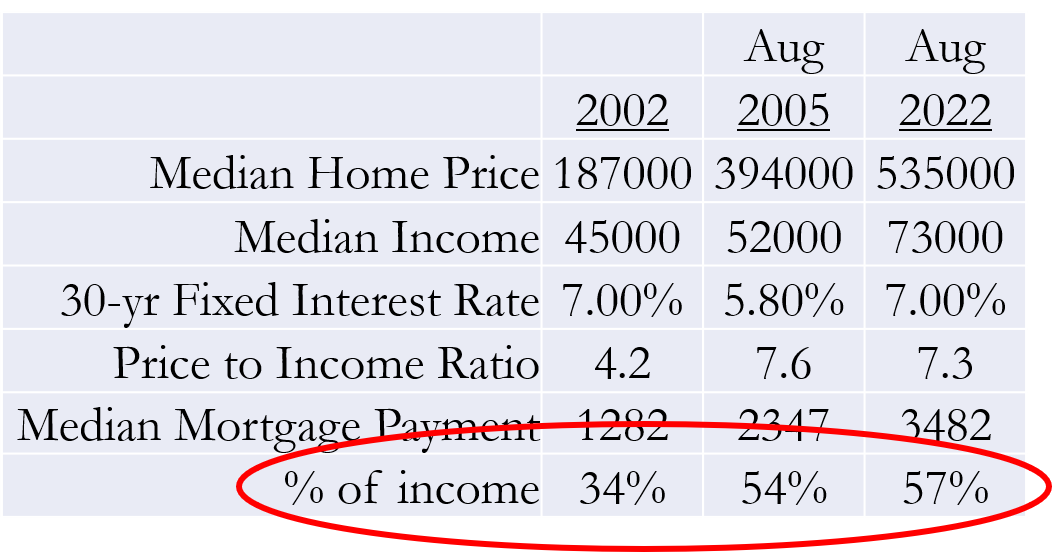

First a brief history overview…over this past summer, annual inflation was running at over 8% and consistently higher than market forecasts. There seemed to be no end in sight for price increases everywhere, including rates for mortgages. As a result, mortgage rates skyrocketed from 5% to nearly 7.5% in 2 months.

That’s when I did my last post on this topic to sound the alarms about housing becoming increasingly unaffordable. I compared the present market to the last time rates hit 7% in 2002 and the last time home values peaked in 2005 to show today’s market was less affordable than either of those eras. This was gauged by the percentage of income going to buying a median priced home by a household earning median income.

I illustrated how either home values would need to fall 21% or rates drop to 4% for the market to come back in balance, and I ultimately forecasted that we would see decreases in both in the months ahead.

That projection has mostly played out, largely thanks to inflation readings falling faster than expected. Mortgage rates have slid back down to 6% and home values have dropped another 9% since August.

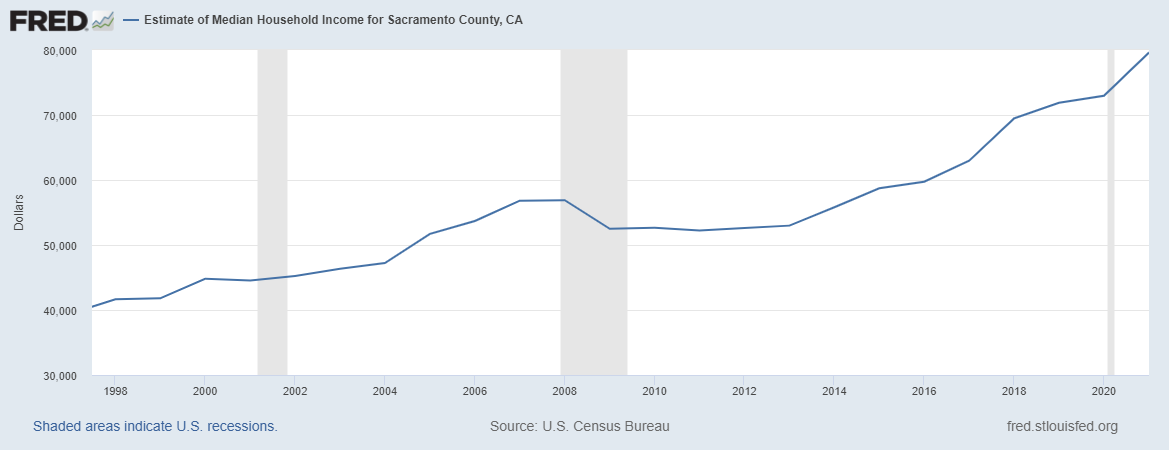

The US Census Department also recently released an updated estimate for Sacramento household median income, which saw an expected increase due to inflation pressures as well.

When accounting for these market changes, the percentage of income going to a mortgage payment is no longer at record highs. In other words, we should not expect home values to continue to fall due to affordability issues. Now, will they still fall anyways? Perhaps they do still fall a bit further because markets don’t always act logically and predictably.

But that’s all the more reason if you’re a buyer and have been waiting to purchase to jump back in the market. These stats show support for current market values, and the short-term projection is for mortgage rates to remain at or below 6%. Many sellers are panicking as the average listing is on the market for 6 weeks and selling for 6% off their asking prices.

These 3 sixes are a literal jackpot sign for buyers entering the market. Thru January we’ve seen signs of the market picking back up and home prices stabilizing, so buyers should feel confident getting out there and ahead of the spring time rush.

Let my team and I help you get pre-approved for financing, find the right home in your area that meets your budget, and negotiate a deal for you in this buyer’s market. We’re here to help you from start to finish, so please reach out with any questions and interest you have on buying a home now or in the future.

Expect more sales, lower rates, and bottoming home values

2022 was a rough year for the real estate market. Interest rates and home values both changed course at the fastest pace on record, causing many potential buyers & sellers to hit the pause button on their transaction efforts. As we enter a new year, sellers likely have been waiting for the rain to finally end to list their homes, while buyers have been waiting for lower rates and home values before jumping back in the market. Will the current “bear” real estate market end? Will a “bull” market return? Read more as I share my insight on what’s ahead for our market (& read all the way to the end for why they are called bear & bull markets!)

The bear market will come out of hibernation (but don’t expect a bull market to return)

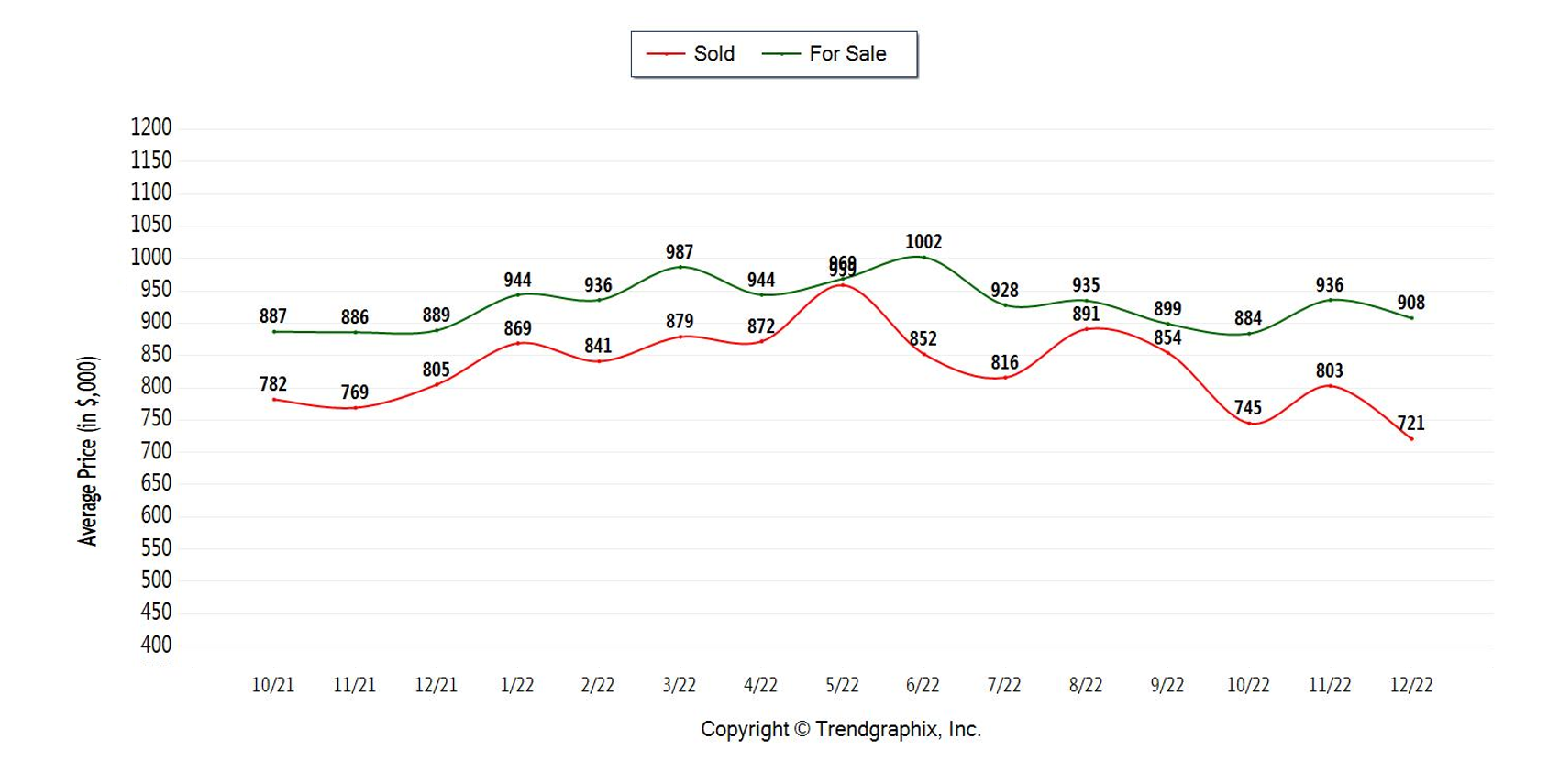

Most regions throughout California have become “bear” markets, meaning home values have fallen consistently and considerably. Take Folsom, for example, where the average home price fell 25% from May to December. That’s a sobering statistic for current home owners considering selling, but keep in mind the current values are still higher than they ever have been if you exclude the insane Covid-related boom. These recent declines are largely due to higher interest rates and hesitant home buyers, but also because of SIGNIFICANTLY fewer home sales. To be precise, the 4th quarter (October-December) was the slowest quarter in over 20 years in Sacramento County, with fewer than 30 homes selling per day in a county comprised of over 600,000 housing units!

Average Folsom home prices over the last 15 months. From the May high of $959,000, the average home price has plummeted to $721,000 (nearly 25%) in only 7 months!

Expect the market to pick back up in 2023 as more sellers put their homes up for sale and buyers eagerly purchase them. Affordability has improved due to declining home values, thus inspiring first-time home buyers to get back into the market. After 3+ years of competitive bidding wars and few homes for sale, buyers are now calling the shots in transactions. The typical listing is selling for 6% less than the asking price, with sellers often paying credits towards closing costs and home repairs. Many buyers will score great bargains on homes this year, but they shouldn’t expect rapid price appreciation to return to the market just yet.

Interest rates will settle down (but don’t expect record lows to return)

Interest rate declines are also helping affordability. Yes, you read that right…interest rates are going down! After peaking at nearly 7.5% in October, 30-yr fixed rates are settling down near 6% in recent days, and likely poised to drop further in the months ahead (more on that in a future post).

While rates aren’t likely to plummet back to 3%, 30-yr rates in the ~5% range will help to stabilize the real estate market and reduce the sting buyers feel when calculating their monthly payments.

Sacramento home values will bottom out (but don’t expect big price gains to return)

The worst is likely behind us with falling home prices. After dropping 2-3% per month since May, Sacramento area home values should find a bottom sometime this year. Rent rates remain high everywhere (1-bedroom apartments are renting for over $2,000/month!), which will help prop up home values as tenants weigh the options between renting and buying. 2023 buyers may risk some short-term losses in equity, but that is a small risk to take for the big rewards of purchasing a home in this strong buyer’s market. After 6 months of price drops, the average listing is on the market for 6 weeks & selling for 6% off the asking price. These 6s may be a troubling sign for sellers, butfor buyers it’s a proverbial jackpot! Get out in the market and let me help you dictate the terms of your next home purchase!

2023 will feel like an awakening after a dormant second-half of last year. If you are a seller, you need to make worthwhile preparations to your property to make it stand out above the competition. If you are a buyer, you need to “start your engines” and follow my top 5 tips from my prior post to get ready to decisively act when the right home comes up for sale. Both sides need to be partnered with an experienced mortgage and real estate broker like me who can navigate you through this changing market. I look forward to helping more clients in the weeks ahead prepare for their 2023 transactions.

PS – Bull & Bear markets earned their names based on how these animals attack. A bull lowers its head and then surges its horns upwards in an attack, hence why a bull market is known as one that is on the upswing. Bears, however, get high and then attack down with their giant paws. When a financial market (like today’s real estate market) is going down in value, its known as a bear market. Now you know!

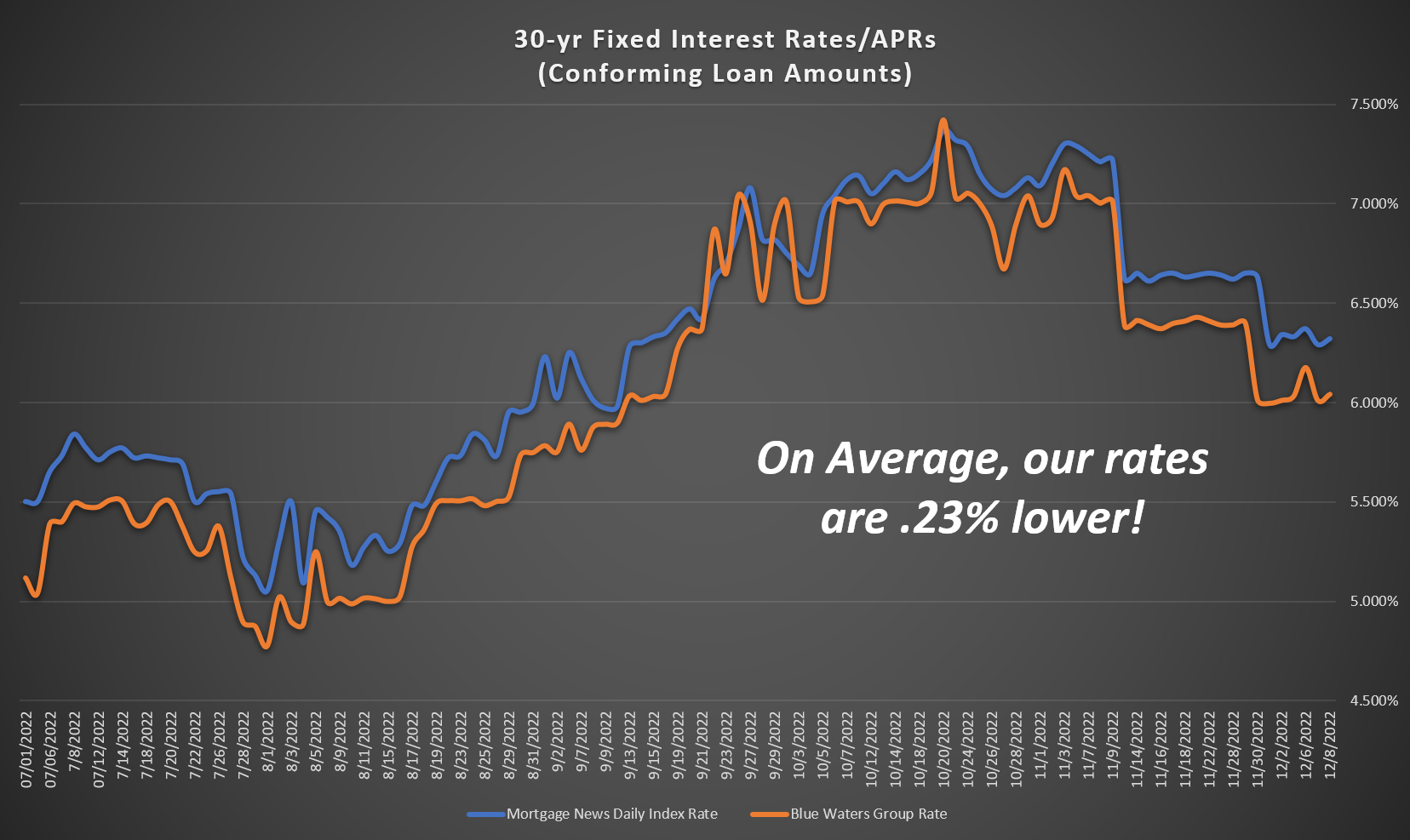

Let’s revisit this chart & show you how we are consistently better than the competition

Mortgage rates dropped over 1% from Halloween to Thanksgiving, making it the best winning streak for rates this year. During that same time period, our lenders dropped their rates by nearly 1.5%, making ours some of the lowest around!

As a mortgage broker, we have the ability to secure the best rates offered by our wide array of wholesale lenders. This means the rate we find for you is generally lower than anything else you may find at a traditional retail bank.

*Rates illustrated are based on a loan amount less than $648,250 with 740+ credit score & 25% home equity

Here is a chart showing how our 30-yr fixed rates* recently compared to the industry at large. The blue line is the Mortgage News Daily Index, a broad sample of rates offered by various mortgage companies, while our available rates are shown on the orange line. You can see our rates have been consistently lower than the industry index, on average, by .23%.

We love doing business as a mortgage broker because we can find the best rates around. We never work with just one bank, because banks are always changing their rates. Sometimes one is overwhelmed so they raise rates to intentionally push business away. Other times they have a “sale” and discount their rates more than others. Our job is to find those opportunities to get you the best interest rate possible.

And what’s even better is you do not pay us for our services; the lender does! When you combine our experience & service with great interest rates, you get the best of all worlds! If you or someone you know has been waiting for a rate decrease to refinance or purchase a home, give me a call.

After spending this year on the sidelines, buyers should be revving up for a purchase in the new year

2022 was an unprecedented year for the real estate market. Interest rates and home values both changed course at the fastest pace on record, causing many potential buyers to hit the pause button on purchasing a home.

As we approach the end of the year, much of that market volatility is now hopefully behind us. Home values have leveled off over the last 60 days after dropping ~12% since spring time, and 30-yr fixed interest rates have slipped back below 6% on growing reports of moderating inflation.

Presently, buyers remain hesitant. In November, fewer than 1,000 homes sold in Sacramento County; the lowest November tally since 2007. Its likely that buyers won’t fully reengage till after the holiday season, but I think potential buyers should be “revving” their engines NOW in preparation for a 2023 home purchase.

I anticipate a very active start to the new year as home values and interest rates continue to normalize. Its imperative that if you are considering an upcoming home sale or purchase that you get your ducks in a row now. Here are 5 things I can help you with NOW to best prepare for an upcoming home purchase:

#1 – Get Acclimated to Market Stats and Trends

Knowing your numbers will help you to confidently negotiate with a seller. Not all neighborhoods are following the general market trends, so work with a professional to know what’s going on in your areas of interest.

#2 – Get Pre-Approved

Knowing what you can afford & understanding your financing options will keep your home search focused & realistic.

#3 – Get Your Financial House In Order

Identify errors on your credit report & oddities on your bank statements that may need attention to make the underwriting & escrow processes easy and predictable.

#4 – Get Your Actual House In Order

Do you need to sell your old home to buy a new home? Sale-contingent offers are more common-place in this current market. Its important to tackle necessary fix-it projects now so you can quickly list your home for sale when you find your next home to buy. Don’t know which projects to focus on? We can help! Even if you are a first-time buyer, knowing your lease terms & getting non-essentials boxed up ahead of time will help you plan your home purchase accordingly and make the process less stressful.

#5 – Get Real With Your Needs & Wants

Its inevitable that a home purchase will require some form of compromise (with your partner, your budget, or both!). Have a written list of what is most important to you & your family in your next home. Having a clear vision & set of priorities will help you be decisive when the right home comes along.

2023 will be one of the strongest “buyer’s” markets of the last decade. Buyers will have the advantage over sellers when negotiating price and other terms. As a broker with over 20 years of experience, I have seen that the best deals go to the clients who are prepared and calculating when buying a home. Don’t let your emotions and impulses drive the process; follow my 5 starting tips now and call on me and my team to help navigate your next home purchase.

-Bobby

Success is where preparation and opportunity meet.” -Bobby Unser, race car driver

It may be time for a cash-out refinance, but time is running out to get the best terms

Total US household debt continues to climb even as borrowing costs rise with higher interest rates, particularly on credit cards. The total debt level recently hit a record amount of $16.5 trillion…with a T!!!

While over $11 trillion is attributed to mortgage debt, that leaves $5 trillion in car, student, and credit card loans. By my account, that averages to more than $40,000 per household in consumer debt! Many of us are facing harder times with the on-going economic slow down along with surging gas and food prices. With credit card balances & their interest rates at all-time highs, it may be time to consider a cash-out refinance to consolidate high-rate loans.

Home values remain reasonably resilient & most homeowners have record levels of home equity. At the same time, mortgage rates are settling down, with our best-priced lenders back in the 5s on 30-yr fixed loans.

Has the economic slowdown forced you to borrow more against credit cards, cars, and education? Borrowing from your equity at a low rate to pay off higher rate debt will lower your overall monthly payments and lower your interest costs over the long-run. I can help you determine the “blended rate” of your various debts, the effective interest rate you’re paying across all of your loans (including your mortgage). If your blended rate is over 5%, then its time to consider a cash-out refinance.

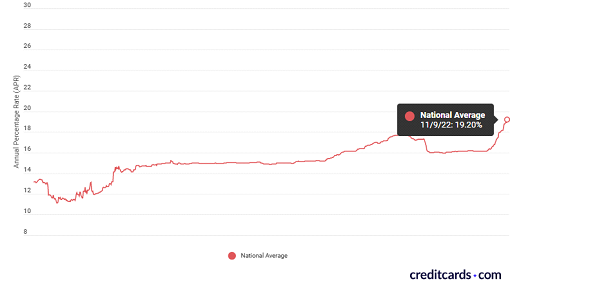

Consider the following graphs…according to CreditCards.com the national average credit card interest rate is nearly 20%, the highest mark in the last 20 years. With The Fed suggesting further increases to the Federal Funds Rate, this will lead to even higher credit card rates.

Meanwhile, mortgage rates have been falling as credit card rates have been rising. 30-yr mortgage rates dipped below 6% this week for the first time since September. Our rates, in particular, continue to be much lower than the industry average (read Our Rates Are Some Of The Best In The Biz).

Let us help alleviate the financial stress of carrying high credit card balances at astronomically high interest rates by refinancing them into a lower fixed rate mortgage. There is a small window this month before cash-out refinances cost thousands higher in fees due to industry-wide changes to these types of loans, so give us a call now & allow us to assess your cash-out refinance options.

**The chart above is for illustrative purposes and not intended to be used as a rate quote. Rates vary based on loan size, credit scores, and many other factors. Give us a call to get a customized and competitive rate quote.**

Major life events will continue to prompt real estate transactions

For the last two years, most home purchases were driven by “wants.” Covid-related isolation made many buyers feel like they “needed” a bigger backyard, a home office, a vacation home, a Red-state zip code…but those were wants, not needs.

With current mortgage rates now over 7%, most existing homeowners may be content sticking with their sub-4% mortgage rate and never moving again. Right?

Think again.

Contrary to recent history, the real estate market is not solely guided by mortgage rates and exuberant home buying trends fueled by reality TV. It’s guided by life; you know, the thing you are constantly planning but inevitably takes an unexpected turn. And its in these turns when people NEED to move to a bigger home, a smaller home, a different state, closer to new work…the list goes on and on.

You never know where life’s next turn may take you

Marriage, job relocation, illness, promotion, divorce, kids, grandkids, death…these events drive the real estate market; keystone life moments that are emotionally charged with excitement, fear, hope or tragedy. As such, its important you and your loved ones enter your real estate transactions with experienced & caring professionals. We know your home purchase or sale is more than a transaction; it’s a significant chapter in your life’s story.

Higher mortgage rates will certainly curtail a homeowner from moving just because they are bored with their current house. But life goes on for the rest of us. Something will come along that will force you to reconsider your living situation. When that time comes, I hope that you’ll give me a call to review things with you. Nearly no one else does what we do: holistically assess your overall real estate position including your current home’s value, your new home buying opportunities, and the mortgage programs available to you.

Life’s unexpected twists & turns may force you to change direction with your real estate affairs, but we will be able to clearly articulate the options available to help you stay on your path.

This year has been a challenging one for mortgage and real estate companies. After years of ultra-low rates & fast-selling homes, 2022 has brought a swift change in market conditions. Some of the biggest mortgage companies in the country are closing up shop, and for the first time in a decade the number of Realtors across the country is declining.

So…you may ask…how is The Blue Waters Group faring? We are certainly having a difficult year as well, but we are not running for the hills. To the contrary, we just signed a lease at a new location in Folsom that will more than triple the size of our office! Our goal is to mentor more like-minded real estate agents and mortgage consultants to provide the utmost care to a growing family of Blue Waters clients. We are incredibly excited to share more details in the months ahead, and host an open house party & other events once we’re all settled in.

Here’s the truth of it…the easy money is gone and so are the ones who were here chasing it. And that’s a great thing for all of us!!! Clients need sound guidance and clear options from experienced and caring professionals, not short-sighted smooth talkers. Only those who are in this field for the right reasons will survive the new market. The Blue Waters Group is here to serve our clients and community regardless of the market conditions, and we are confident you will be referring us more than ever in the future!

Thank you for your support of our business these first 10 years in our “starter” office. We look forward to the opportunities our new location will provide our team & clients!