The federal government shut down began at 12:01 AM today. For the first time since 2018, US Congress has failed to pass a budget, preventing many non-essential operations from functioning. How will this impact every day Americans and, more specifically, the mortgage and real estate markets?

Federal Loan Programs – Most home loan programs involve the Federal government in some form or fashion, so it’s possible loan programs will be impacted by a shutdown. The likeliest problem areas will be obtaining Flood Insurance Policies from FEMA and Tax Transcripts from the IRS. Most other underwriting and funding functions should continue as usual.

Interest Rates – The last shut down in 2018-2019 lasted for 35 days, the longest in modern American history. During that time, the average 30-yr fixed mortgage rate dipped initially, but ultimately ended up at a similar level as at the beginning of the shut down. After the shutdown, mortgage rates dropped nearly ½% in the following two months. That sudden rate drop in 2019 was largely due to recession fears, trade wars, and a policy shift from The Fed. Huh…sound familiar??!! Those are the same headlines in today’s market! Will a similar outcome occur this time around? It’s certainly possible!!!

Real Estate Market – While the shutdown won’t have a direct impact on most real estate transactions, it will potentially cast doubts over the real estate market as a whole. Will buyers and sellers alike hold off on making major financial decisions as a result of the shutdown? Surely there are millions of people employed by the Federal government who may feel uneasy about their jobs, but I think those of us outside of government employment will also become unsure about what the fallout of this government shutdown will look like. Uncertainty will squeeze the housing market, so lets hope the shutdown is short and a bipartisan agreement is reached quickly.

I’m sure you’ve heard the news…mortgage rates have finally been falling! But if you’re sitting on a high mortgage rate should you hold off on a refinance until after the upcoming Fed press conference?

Many people expect The Federal Reserve to lower the federal funds rate 1/4-1/2% on September 17th. But what most people misunderstand is this has no bearing on when or even if mortgage rates drop. Mortgage rates have already fallen nearly ½% in the past 30 days due to the same market conditions that are prompting The Fed to cut their rate next week. Mortgage rates don’t wait for Fed policy; mortgage rates change in real time as market conditions change.

Here’s my advice…if your mortgage rate is currently at 7% or above and you have good credit and home equity, look into refinancing now. Don’t get greedy and hope rates get even better next week. It’s worth pointing out that the last time The Fed lowered their rate, mortgage rates actually increased. As the old adage goes, better to take the bird in the hand, instead of two in the bush.

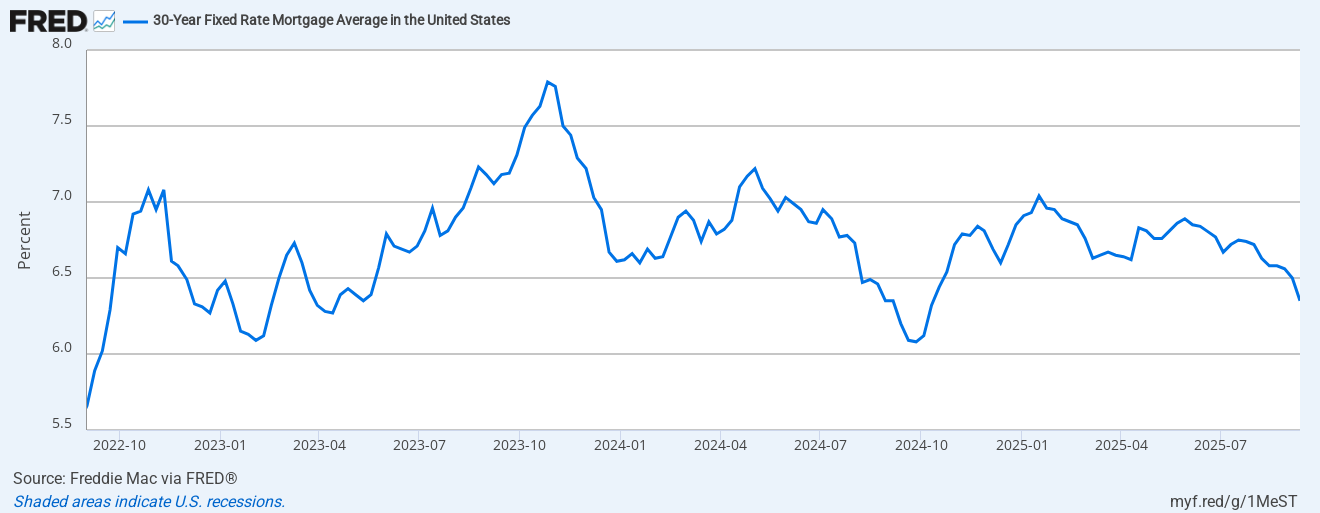

As the chart below illustrates, mortgage rates have not dipped below 6% in the past 3 years. And each time they approach that barrier, they bounce HARD in the other direction, rising 1.0-1.5% in the following months. We are testing that 6.0% barrier again. Will it break through this time? Or get rejected for the third time in three years?

But, if your mortgage rate is already in the 6s and you’re not interested in shortening your term to a 15 yr loan, then “roll the dice.” Sit tight and see if rates fall further. I wouldn’t count on it happening right away, but there’s always that small chance lower rates are on their way.

I’ll be working this weekend and can even lock your refinance rate during after-market hours. Hit me up if you want to explore your refinance options with an experienced & local mortgage broker before the high volatility of next week’s Fed meeting impacts the financial markets.

We’re thrilled to share that we have been nominated again as Best Mortgage Broker and Best Real Estate Team in Style Magazine’s 2025 Best of the Best Readers’ Choice Awards!

You may recall we earned awards in both categories in 2024, and we are looking to repeat these high honors. As a small (but mighty!) team, we pour our hearts into helping you buy, sell, and finance your home—offering top-notch service and interest rates that make you and your wallet smile. It’s our passion, and it means the world to be recognized for what we love to do.

Now we need a quick favor that’ll only take a couple of minutes—but gives you lifetime bragging rights for helping us achieve the highest honor: 1st place in both categories!

👉 To cast a valid vote, you’ll need to vote in at least 10 categories.

To make it easy, we’ve put together a cheat sheet with other incredible local businesses we admire and think are vote-worthy, too. But of course, feel free to choose your own favorites!

Your support truly means everything to us. Thank you for being such an important part of our journey—we couldn’t do this without you! 🏡💛

I am very excited to pass along a big announcement from two of my biggest competitors. Why?!? Let me explain.

Earlier this week, Rocket Mortgage, one of the largest mortgage companies in the country, spent nearly $2 BILLION to acquire Redfin, one of the biggest names in real estate. You may recall that Re/Max (the largest real estate brand in the world!) did something similar back in 2016 (I wrote about it then too).

They aim to create a “one-stop-shop” experience for clients so they can buy, sell, and finance homes from a single source. Hmmmm, why didn’t I think of that? 😉

The biggest brand names in real estate are joining forces and copying my one-stop-shop business model. Some may say this trend of big companies creating end-to-end consumer “ecosystems” is bad for my business. Should I be concerned about my market share?

Perhaps, but the overwhelming feeling I have is one of flattery. I’m absolutely flattered that the likes of Rocket Mortgage and Redfin, publicly-traded companies valued at BILLIONS of dollars, are trying to emulate us!

The Blue Waters Group has believed from our very beginnings that the customer benefits from competent and compassionate advisors who can offer both mortgage and real estate services. With Rocket Mortgage & Redfin literally spending billions of bucks, no longer is our business model the obscure alternative; it is the one that leading industry players are striving for. No longer is our platform one that I need to defend with blog posts titled Is What I Do Legal?; it is the one that’s copied by others.

We are still unique from these big company aspirations in that our associates are able to offer both mortgage and real estate services (all of us are licensed both as mortgage loan originators and real estate agents) while Rocket simply hopes to pair mortgage and real estate services more efficiently by providing them under the same corporate umbrella. Nevertheless, this week’s move by Rocket Mortgage & Redfin further validates the craft I’ve been honing for nearly my entire career.

Working as both a mortgage broker and REALTOR is not an easy task, but with a 22-year head start on these firms and others who are sure to follow suit, I’m confident The Blue Waters Group will continue to be imitated but never duplicated!

Over the past 15 years, I’ve provided an annual forecast of the mortgage and real estate markets. Generally, I speak to three main characteristics: housing supply, buyer demand, and interest rates.

This year, it’s all about the rates. If 30-yr mortgage rates remain at 7% or higher, housing supply and buyer demand will remain anemic. If they fall below 6%, we will see a flood of both buyers and sellers enter the market. Much of 2023 & 2024 saw rates largely stay within the 6-7% range, which led to generational-low transaction count and record-low affordability levels.

As such, it makes sense to focus my forecast on where interest rates may be heading in 2025.

Who Controls Interest Rates?

Many people are led to believe mortgage rates are controlled by select individuals, such as bank CEOs, The Federal Reserve Board (affectionately known as “The Fed”), or the sitting president (not sure what his affectionate nickname is at the moment). This is not correct!

Mortgage rates are actually controlled by the buyers and sellers of mortgage backed securities. In plainer words, mortgage rates move by investors trading mortgages. There is no man behind the curtain; no key players puppeteering rates, nor a president successfully demanding interest rates “to drop immediately“.

Instead, rates move based on risk & opportunity cost for these free-market investors. Let’s talk briefly about each of these factors.

First off, the biggest risk factor for a mortgage trader is inflation. Inflation eats away at the value of money, so when inflation increases traders don’t want to buy ultra-low rate mortgages. If they buy a mortgage bond with a 3% fixed rate, but inflation is at 4% they are actually losing money.

And opportunity cost is simply a question of can a trader buy an alternative investment with a higher rate of return & lower risk. So, no smart trader would buy a 3% mortgage when there are risk-free money market accounts offering 4% savings rates.

Below are the issues mortgage traders will be focused on in determining how much in mortgages they want to buy and at what interest rates.

Factors in 2025 that will push rates DOWN

Slowing Economy – Many sectors of our global economy have slowed down in recent quarters. Many factors could have contributed to this (political uncertainty, rising cost of goods/services, ), but generally interest rates fall during sluggish economic times. The primary driver of recent Gross Domestic Product (GDP) growth was personal consumption, but I believe personal consumption will slow in 2025 as households are forced to tighten their financial belts. Credit card balances are at record highs and continue to climb (check out my prior post about the alarming levels of household debt).

Lower Inflation – Rising prices on everything took a toll on most of the world in 2022-2023, but things are starting to ease. Inflation rates are now slightly over the historical trend and The Fed’s preferred level of inflation. Don’t expect prices of things to fall, but if they hold at near-constant levels then mortgage rates should decline.

Higher Unemployment – If fewer people are working, it is a sign of a weakening economy. While statistics continue to show 100-200K new jobs being created every month, this could change dramatically in the coming months. The largest employer in the US (the federal government itself) is mandating most employees to return to the office for work and looking to significantly scale back the total number of government employees. This could drastically change the employment picture, and push the unemployment rate up.

Factors in 2025 that will push rates UP

Long-term Tariffs – President Trump is using Executive Orders to impose or threaten tariffs on certain countries and certain products. Tariffs are essentially an added tax on goods that are made in a foreign country. Some people think this added cost will be absorbed by the foreign company who is importing the goods, but this is rarely the case with tariffs. The tariff is typically added to the cost of the item, meaning the end consumer (Americans) will incur these tariff expenses. If tariffs become more of an entrenched part of Trump’s foreign policy rather than a short-term negotiating tactic, it will drive up inflation and interest rates with it.

Smaller Labor Force – Between deportations and baby boomers retiring, the number of available workers could decrease. With fewer workers, employers will need to increase wages to entice people to the workforce. This will fuel the flames of inflation (as it did when we came out of the deepest economic trenches of the pandemic) and push interest rates up higher still.

Growing Government Debt – Our country is in debt more than ever before. Presently, we carry over $30 TRILLION in debt, which is over 120% of our Annual GDP. That percentage is similar to levels seen at the end of World War II. It made sense we were in debt up to our eyeballs after fighting a World War for 4 years, but this is the first time we’ve been at these levels during peacetime! Our government debt is sold to investors via Treasury bonds, and the more we go into debt the more we have to entice them to keep buying our bonds. This enticement is in the form of higher rates of interest earned by the investor (and paid by the borrower). If rates of gov’t bonds increase, then mortgage rates will follow suit as well.

What Will Win The Tug-of-War?

2025 will see these pressures pull against one another, and neither will be a clear-cut winner. I do believe the downward pressures will slightly win out, as some of the upward pressures (tariffs in particular) also tend to slow down an economy, which should lead to lower rates. Overall, if you start hearing the R-word (“recession”) thrown around in 2025, expect 30-year rates to finally dip below 6% by the end of this year.

If mortgage rates do considerably improve, there will be more real estate transactions but not necessarily higher home values. It is expected more homes will come up for sale (both new construction and resale homes), which will keep home values somewhat in check.

If mortgage rates end up increasing above 7%, then we could see home values fall. With affordability already out of reach for so many potential home buyers, worsening conditions will further reduce the already anemic levels of demand currently seen.

Do you have thoughts or insights to share about your local real estate market? Leave them in the comments section below.

Here are the factors to consider if you have a rate over 6%

Clients often ask me about “timing the market.” In other words, is there a way to get the best price or lowest rate based on WHEN you buy/sell/refinance? Last year I researched historical data of the past decade and posted about the best times of year to buy and sell homes in Sacramento. It revealed seasonal trends that show Winter (not Summer!) is the best season for sellers and Fall (right now!) is best season for buyers. Even Realtor.com supports my research in their own recent report that claims THIS WEEK (September 29-October 5) will be the best week this year to buy a home!

But how about timing a refinance? Is there a way to perfectly time the financial markets to assure you get the lowest possible mortgage rate on a refi? Let’s dive in and discuss!

As you may know, mortgage rates move every day. Much like stock prices, their daily gyrations are unpredictable even though many market experts spend their lives studying and predicting them. But surely there must be a way to know if mortgage rates will go up or down in the near future, right???

WRONG!!! We only need to look back a couple of weeks for clear proof of the erratic nature of mortgage rates. On September 18th, The Federal Reserve officially lowered the Federal Funds Rate by ½%. Many expected mortgage rates to follow suit, but surprisingly mortgage rates actually increased slightly upon The Fed’s actions.

Mortgage rate changes do not have seasonal trends the same way as the real estate market. To prove this, I studied data of 30-yr mortgage rates from the past 40 years, and found that mortgage rates don’t drop more frequently in one time of year over another. I recorded all of the months where mortgage rates fell, and noticed these tallies were evenly spread out throughout the year:

Season

# of Months w/ rate drops (since 1984)

Spring

73

Summer

52

Fall

76

Winter

77

As you can see, there is no season that significantly stands out above another. In fact, Spring, Fall and Winter had nearly the identical number of months that experienced rate decreases.

As an easy visual comparison between the real estate and mortgage markets, look at the rhythmic, predictable nature of the chart on the left showing home sales over the past 10 years (generally peaks in 2nd quarter; bottoms in 4th quarter) to the chart on the right showing 30-yr mortgage rates over the same time period (no pattern whatsoever).

Real Estate Sales look like a heartbeatMortgage Rates look like a seismograph!

If seasons are not an indicator, then perhaps significant events could be a tell-tale sign for mortgage rate movements…presidential elections, perhaps? Many people believe major elections create uncertainty in the financial markets, and generally mortgage rates fall in times of uncertainty. As a result, I’ve had some clients who could benefit from a refinance today gamble their guaranteed savings of today by holding off on a refinance decision until after this year’s upcoming election. Risky move, especially given the history of what mortgage rates do (or don’t do!!!) in election years.

I looked back at mortgage rates since 1980 and tracked the direction of rates in the months leading up to November. I found that in these 11 presidential cycles, 5 of them experienced rate increases while 6 saw decreases; a mixed bag with no clear trend. Most of these periods saw modest changes, with the average rate change being less than .5% over the 10-month pre-election intervals.

If the sun and moon and stars and elections can’t help us predict interest rates, then what should we look to instead??? Here’s my honest advice…ignore all of the “signs!”

Put away the tarot cards and pick up a calculator! When deciding when or if to refinance, stick to these simple factors:

What will today’s interest rate save me?

What will today’s interest rate cost me?

How long do I plan to have this loan?

Generally speaking, most of my current clients are choosing to refinance if they can recoup the closing costs within 12 months of their monthly savings amount. For example, if a proposed refinance costs $3,000, then it would make sense in most cases to do so if you can save $250/month or more. Doing so is allowing them to save money now, but keep the opportunity to refinance again if rates continue to fall in the future.

While these are straightforward calculations, the pros & cons of a refinance can be nuanced and best talked through with a trusted professional. As mortgage rates have fallen in recent months, aggressive marketing campaigns aimed at pressuring homeowners to refinance have increased dramatically. Don’t let an inexperienced sales call center guide you through an important financial decision; reach out to me to discuss your options.