Let’s Get Real about Zillow. It is not a public information service nor is it a real estate firm. Zillow is a for-profit advertising company.

Much like Google, when you get search results, the first items or people aren’t necessarily the best ones. They’re simply the ones that paid the most to be at the top of the list.

If you want unbiased and unfiltered information about listings or service professionals in real estate, use the website of a REALTOR. Search all listings in the greater Sacramento area using the link in my bio. No advertising or sponsoring will alter the results of your search.

Let’s Get Real…Did your REALTOR attend the home inspection on your last transaction? Why the heck not??!!

It’s such an important step in the buying process; I make a point of being at every one. It may be a big time investment, but it’s one of the best ways to advocate for my buyer clients.

Let’s Get Real about IMAGE in Real Estate. Make sure you don’t fall for flashy marketing and false self-promotion that makes a REALTOR’s image suggest they’re more successful and valuable to you than they truly are. Look for EXPERIENCE and AUTHENTICITY!!!

Let’s GET REAL about a slower real estate market. A REALTOR shows their true value when a home doesn’t sell right away. Should they just tell a seller to have patience or say “just trust me?” 🤦♂️

NO WAY!!! A good REALTOR should systematically track the vital signs of their listings regularly to gauge marketing activity levels. Not many do it, but for me it’s a critical way to keep sellers informed and to counsel them when considering price reductions.

Let’s GET REAL about whether REALTORs are more focused on the revenue FROM YOU or the relationship WITH YOU. When I work with new clients I don’t always get a commission, but I always try to earn their trust. I know a genuine relationship will always lead to referrals and other business opportunities in the future.

Let’s GET REAL about…Buying New Homes! Never forget that the builder’s sales office and in-house lender work for the builder, not you!

My latest client learned the hard way of the many pitfalls of buying a brand new home. I was glad to come into the transactions late to get him a great rate and restore some trust back into the transaction.

Before looking at model homes, reach out to me and learn why you should have your own REALTOR and mortgage professional on your side when buying a new home.

Lets GET REAL about…Paperwork! Most of us hate it, but managing it, presenting it, and explaining it are crucial to a successful real estate transaction. Contract mastery may not be a skill emphasized on your favorite reality real estate TV show, but don’t hire a REALTOR that can’t effectively explain the paperwork you’re being asked to sign.

If your credit card balances are creeping up on you, it may be time for a cash-out refinance

Total US household debt continues to climb even as borrowing costs rise with higher interest rates, particularly on credit cards. The total debt level recently hit a NEW record amount of $17.29 trillion…with a T!!!

$1.08 TRILLION is attributed to credit card debt! Many of us are facing harder times with the on-going economic slow down, lingering inflation, and the resumption of federal student loan repayments. With credit card balances & their interest rates at all-time highs, it may be time to consider a cash-out refinance to consolidate high-rate loans.

Home values remain reasonably resilient & most homeowners have record levels of home equity. Even with elevated mortgage rates, it may be better to roll higher rate credit card debt into a new mortgage balance.

Has the economic slowdown forced you to borrow more against credit cards, cars, and education? Borrowing from your equity at a low rate to pay off higher rate debt will lower your overall monthly payments and lower your interest costs over the long-run. I can help you determine the “blended rate” of your various debts, the effective interest rate you’re paying across all of your loans (including your mortgage). If your blended rate is over 7%, then its time to consider a cash-out refinance.

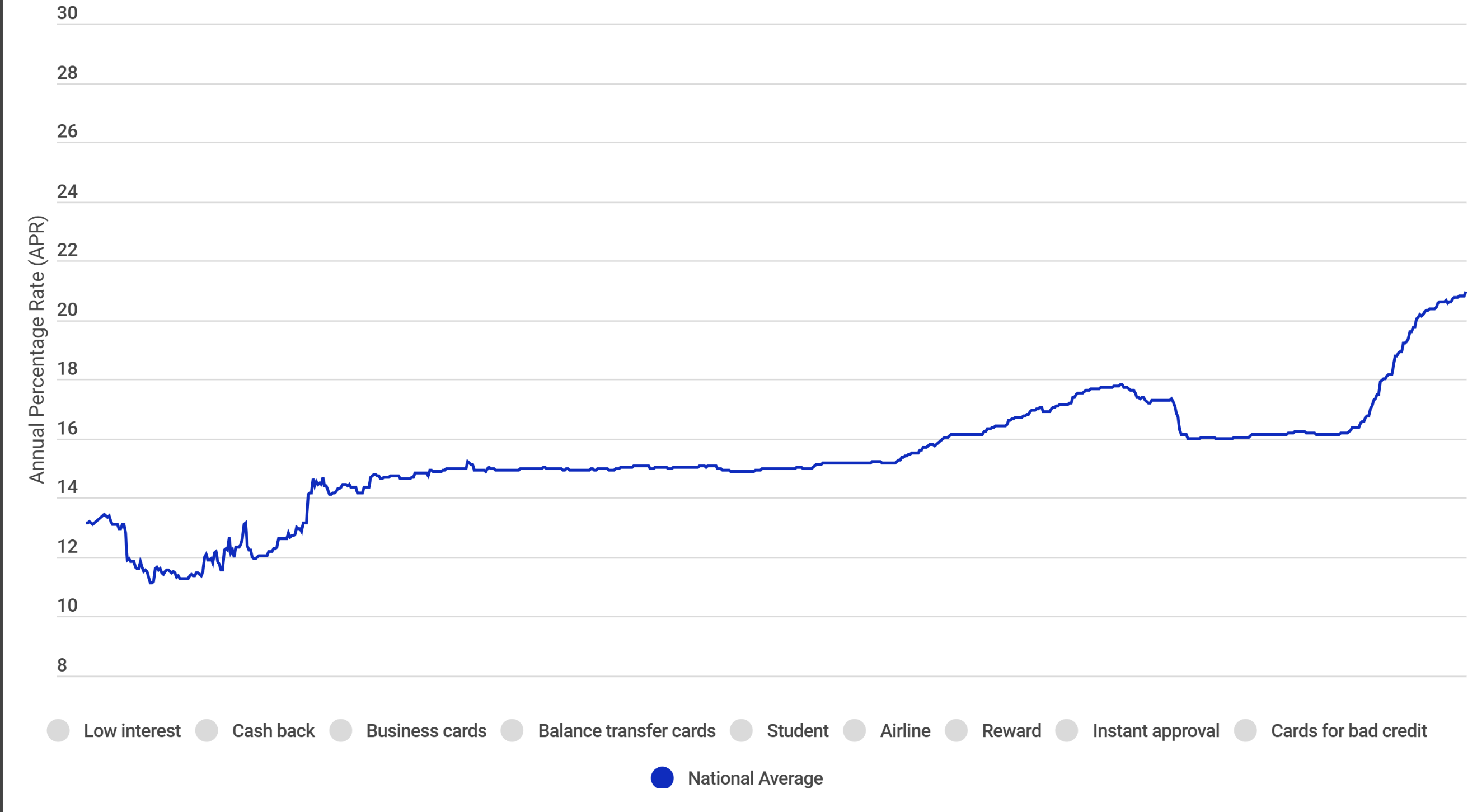

Consider the following graph…according to CreditCards.com the national average credit card interest rate is over 20%!. With The Fed suggesting they don’t plan to reduce the Federal Funds Rate any time soon, this will lead to high credit card rates for some time.

Let us help alleviate the financial stress of carrying high credit card balances at astronomically high interest rates by refinancing them into a lower fixed rate mortgage.

Let’s GET REAL! Being a REALTOR is not about rolling up to a mansion in a Maserati and walking billionaires through homes that sell themselves. It’s about helping everyday clients build their wealth and futures, and that often means you roll up your sleeves to help a first-timer buy a fixer.

Let’s GET REAL! A good Realtor is not the one that GETS your ATTENTION, but rather the one who GIVES you VALUE! This week, I am launching a campaign called “Get Real in Real Estate”…short reels that share real stories that make real impact in real estate transactions. Join me in valuing sincere substance over fake flash.