The last two weeks have been filled with dramatic headlines about our financial markets and global economy. The Fed had an emergency meeting, stock trading was halted for a brief period, and US government bond rates hit record lows. The markets have been in “panic” mode. I’ve always said mortgage rates improve when there is bad news, so mortgage rates are surely in a free-fall, RIGHT???

The last two weeks have been filled with dramatic headlines about our financial markets and global economy. The Fed had an emergency meeting, stock trading was halted for a brief period, and US government bond rates hit record lows. The markets have been in “panic” mode. I’ve always said mortgage rates improve when there is bad news, so mortgage rates are surely in a free-fall, RIGHT???

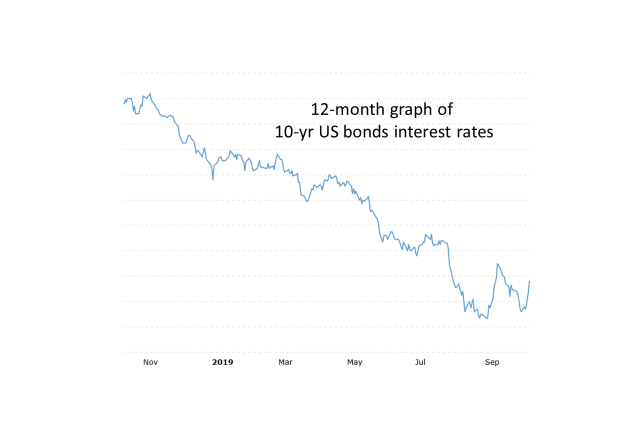

In short, no. Mortgage rates don’t tend to move as quickly as other markets during extreme swings. For example, the rate on 10-yr US bond rates fell .42% last week while 30-yr mortgage rates fell only .08%. There are a number of reasons for this inconsistency, but the point worth making here is that mortgage rates are not in a free-fall…yet!

I believe mortgage rates will fall further in the near future, and last week’s volatility is a clear reminder of just how fragile our economic markets have become. We have spoken to a ton of clients in recent days, and most are deciding to wait for lower rates before taking action. I think this is a wise move for a number of reasons.

First off, significant mortgage rate declines tend to lag behind other market movements. If the world economies and governments continue to grapple with the spread of Covid-19, it will give mortgage rates a chance to “catch-up” and fall further.

Secondly, I believe the financial markets are fatigued and vulnerable to further volatility. Much like a heavyweight boxer in the twelfth-round, it doesn’t take much of a hit to knock out an exhausted fighter. The US Stock market has been on its longest “bull” run in history; it can’t go on forever. The recent market hysteria over the Covid-19 fears and of a potential price war in the oil markets prove it doesn’t take much for the current markets to get scared. I strongly believe the world’s financial markets are “on the ropes,” and the next knock-out punch will be coming soon.

Finally, it rarely pays off to chase markets. A few lucky clients did lock in great interest rates last week amidst the crazy market swings, but most of them had already been in previous conversations with us about a transaction. Thus far this week we’ve seen the markets “rebound” and give back much of the rates drops experienced last week. Rather than regret the missed opportunity of chasing last week’s market, I would advise everybody else to get ready to pounce on the next opportunity. Luck favors the prepared, so begin discussions with us now about potential refinance goals. Doing so will allow us to monitor the markets for your particular situation, and swiftly act when the opportunity presents itself.

Please give me a call or email so we can set up a 10-minute phone appointment. I’ll be working nights and weekends as needed in the coming weeks, so I look forward to finding a time and method to communicate with you soon.

Its not easy for a small-business owner to take time away from their company. If you ask other entrepreneurs, most would tell you they’ve never left for more than a couple of weeks, and even then were handcuffed to their cell phone just in case they were needed. Its common for an owner to be needed; after all its their company! Who else is going to handle the emergencies and tough decisions?

Its not easy for a small-business owner to take time away from their company. If you ask other entrepreneurs, most would tell you they’ve never left for more than a couple of weeks, and even then were handcuffed to their cell phone just in case they were needed. Its common for an owner to be needed; after all its their company! Who else is going to handle the emergencies and tough decisions?

![USA and China trade war[1]_ US of America and chinese flags crashed contain](https://mattsmemos.com/wp-content/uploads/2019/08/usa-and-china-trade-war1_-us-of-america-and-chinese-flags-crashed-contain-e1565976584261.jpg?w=660)