Let’s Get Real about BIG BANKS! They have big-time overhead expenses, so they have to earn big-time interest on their loans. For the best rates, skip the big banks use the services of a mortgage broker like me.

This is not about supporting local or shopping small. This is about getting the best deal possible on your next home loan!

Click on this link to read about how the rates I offer my clients tend to be nearly 1/4% lower than the average national mortgage rates!

Let’s Get Real about IMAGE in Real Estate. Make sure you don’t fall for flashy marketing and false self-promotion that makes a REALTOR’s image suggest they’re more successful and valuable to you than they truly are. Look for EXPERIENCE and AUTHENTICITY!!!

Let’s GET REAL about…Buying New Homes! Never forget that the builder’s sales office and in-house lender work for the builder, not you!

My latest client learned the hard way of the many pitfalls of buying a brand new home. I was glad to come into the transactions late to get him a great rate and restore some trust back into the transaction.

Before looking at model homes, reach out to me and learn why you should have your own REALTOR and mortgage professional on your side when buying a new home.

If your credit card balances are creeping up on you, it may be time for a cash-out refinance

Total US household debt continues to climb even as borrowing costs rise with higher interest rates, particularly on credit cards. The total debt level recently hit a NEW record amount of $17.29 trillion…with a T!!!

$1.08 TRILLION is attributed to credit card debt! Many of us are facing harder times with the on-going economic slow down, lingering inflation, and the resumption of federal student loan repayments. With credit card balances & their interest rates at all-time highs, it may be time to consider a cash-out refinance to consolidate high-rate loans.

Home values remain reasonably resilient & most homeowners have record levels of home equity. Even with elevated mortgage rates, it may be better to roll higher rate credit card debt into a new mortgage balance.

Has the economic slowdown forced you to borrow more against credit cards, cars, and education? Borrowing from your equity at a low rate to pay off higher rate debt will lower your overall monthly payments and lower your interest costs over the long-run. I can help you determine the “blended rate” of your various debts, the effective interest rate you’re paying across all of your loans (including your mortgage). If your blended rate is over 7%, then its time to consider a cash-out refinance.

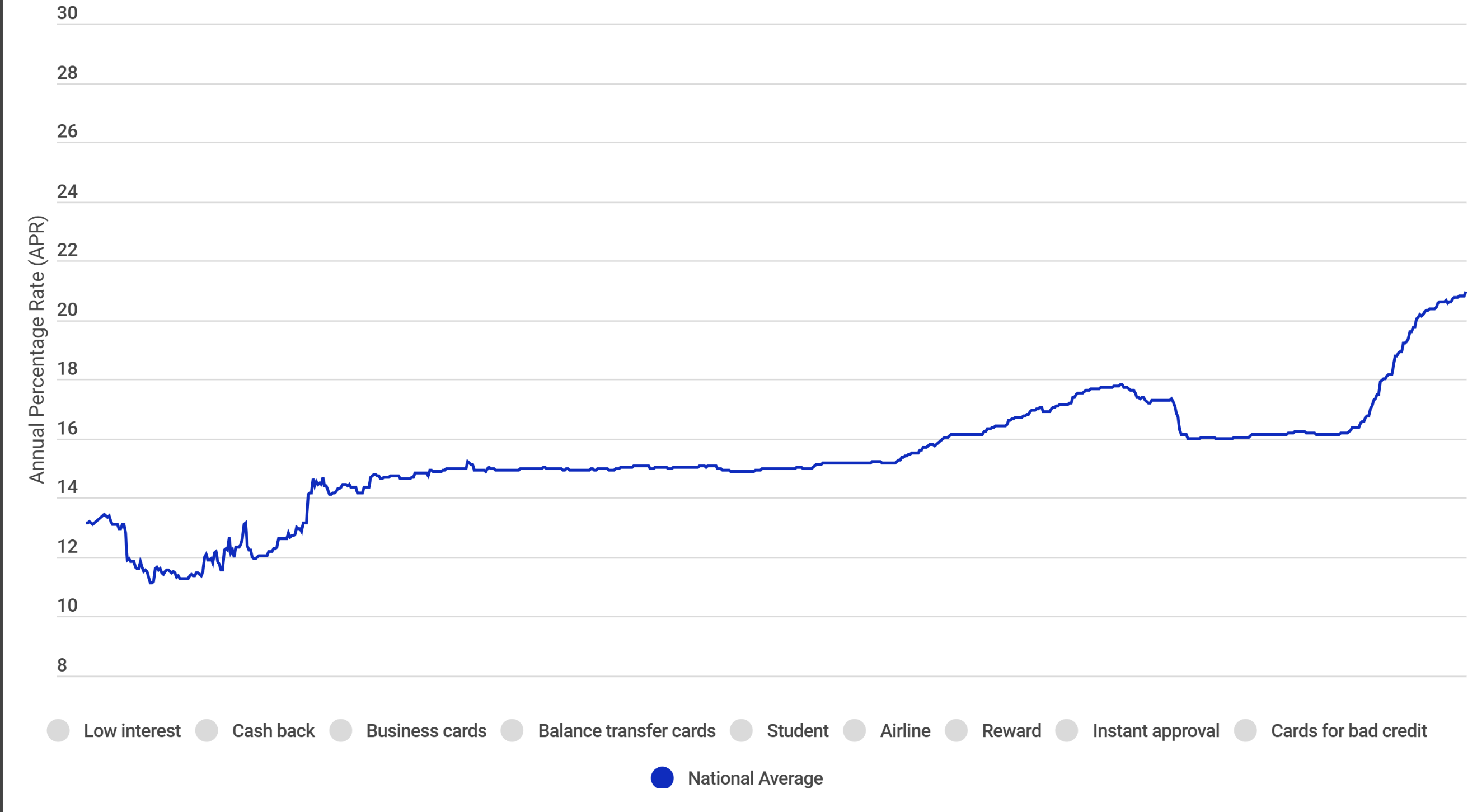

Consider the following graph…according to CreditCards.com the national average credit card interest rate is over 20%!. With The Fed suggesting they don’t plan to reduce the Federal Funds Rate any time soon, this will lead to high credit card rates for some time.

Let us help alleviate the financial stress of carrying high credit card balances at astronomically high interest rates by refinancing them into a lower fixed rate mortgage.

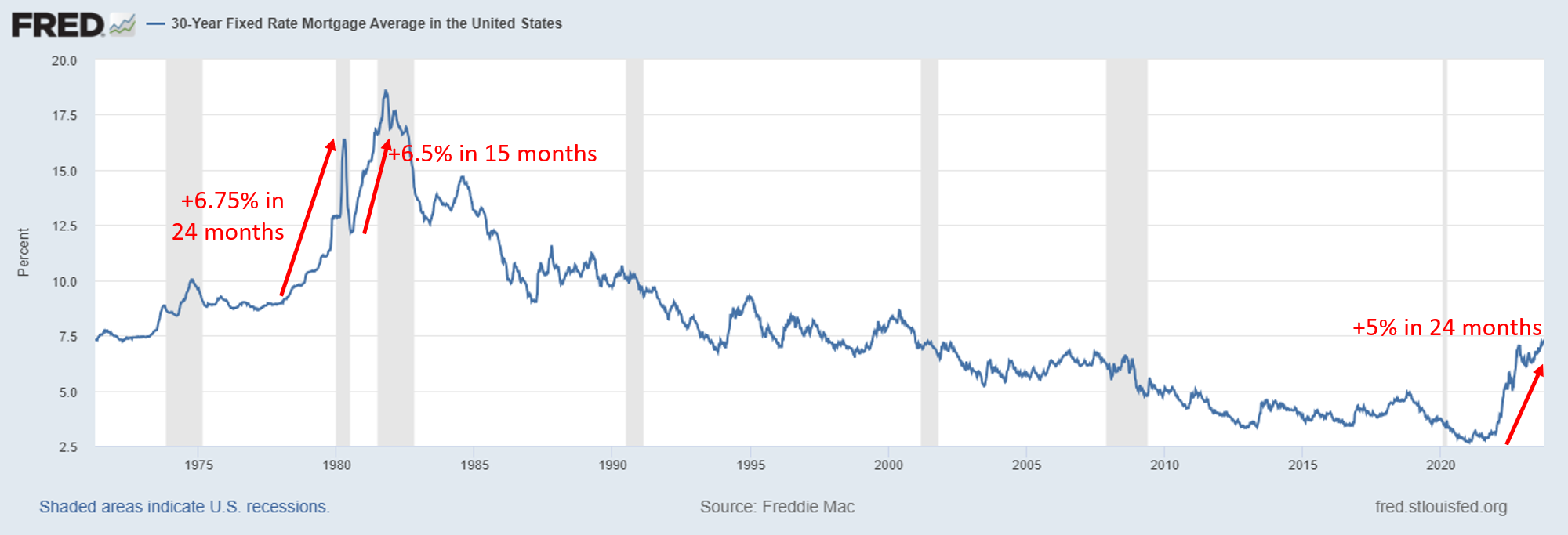

Mortgage rates have officially shot up to their highest levels of the 21st century (that sounds a tad sensational, but its true). Some 30-yr fixed rates are flirting with 8%, over five-percent higher than the all-time lows seen two short years ago. You have to go back to the late 70s & early 80s to see a steeper increase in mortgage rates. Yikes!

These higher rates are making homeownership unaffordable for many. For others, the sticker shock of the monthly payment is too painful to look at, so they continue to rent instead of buy. We covered how this is a poor decision for building long-term wealth at our home-buying seminar last month, but no time to hash that out again in this post.

For the brave buyers who can persevere in this market, they may be facing very favorable conditions in the short months ahead and wonderful appreciation opportunities in the long run. As others turn and run, buyers in today’s market are experiencing much less competition from other buyers, and negotiating with sellers who are beginning to panic as we approach the slower winter months. While no one loves to pay truckloads of interest to the bank, it is worth noting that these higher rates are currently creating a more mellow, favorable market for buyers.

During the 2020-2021 market craze, it was common to have 5-10 competing offers on a listing. In Folsom, for example, the typical listing fetched a price 5% OVER the asking price. Buying a home in that sort of market is frustrating & disappointing, as you have very little control over the outcome of any offer you may write on a home. I believe that type of market craze will return when interest rates drop, but for the moment persistent buyers have the competitive advantage over motivated sellers. Buyers are in the driver’s seat for the next few months!

While its obvious to say higher rates are everyone’s enemy, for some home buyers they should consider them a friend…or at the very least a frenemy!

Here’s a bold game plan to consider if you are a would-be homebuyer…buy now to lock in your home price and then hope to refinance to a better interest rate once rates come down. When rates do eventually settle down, it will likely push home prices up again as more buyers return to the market. Get in front of that wave if you can afford today’s rates & monthly payment!

If you have considered buying a home, then you should read some of my recent posts. There’s one about the benefits of buying a home in the Fall. Another speaks to how mortgage rates will likely drop in the near future. Again, the masses are waiting to buy until rates drop. Consider going against the herd by buying now and refinancing later. Doing so will have far greater long-term benefits, even if the sting of today’s higher rates hurts for the moment.

Once we’re in a recession, and one is coming very soon

In my last post I shared that I see a recession brewing, leading to lower mortgage rates. Well, I think the stage is being set for our next recession right now. Here are 5 big story lines that just came out this week that will lead to slower economic growth (& thus lower mortgage rates!):

#1) Ongoing union strikes – the auto industry strikes are intensifying according to reports from earlier today, so this will slow down a cornerstone of our economy to the tune of $500 million a day in lost productivity.

#2) Government shutdowns – Congress avoided a shut down on Oct 1 by kicking the can down the road with a 45-day budget. But the unprecedented ousting of Speaker Kevin McCarthy could have a greater tumultuous impact on our government operations than a run-of-the-mill budget standoff. Regardless, a prolonged shutdown or inefficiencies within Congress in the coming weeks will impact economic output and further deteriorate the world’s faith in US fiscal responsibility.

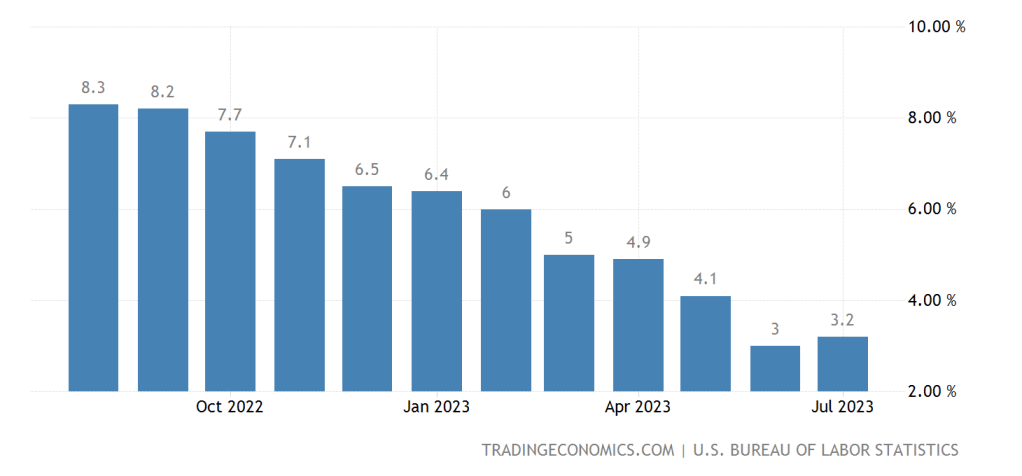

#3) Inflation is cooling – the latest core Personal Consumption Expenditure index came in at a .1% monthly increase, below expectations and heading in the right direction. This is a sign The Fed’s policies are working at slowing the economy and tipping things into recessionary territory.

#4) Student loan payments resume soon – nearly $1.6 trillion dollars in student loans will resume repayment status on Sunday (Oct 1st). After a 3.5 year reprieve, over 40 million Americans will now be tightening their purse strings as more of their monthly budget will go to paying their student loans.

#5) surging oil prices – gas prices are rising at an odd time of year (after Labor Day). Other than during the initial outbreak of the war in Ukraine, gas prices have never been higher. This will crimp consumers spending habits as we enter the important holiday season.

Many economists believe consumer spending has been what’s propped up our economy in recent months despite rising interest rates. Well, I believe that comes to an end this coming quarter, and a lousy holiday shopping season will be the beginning of a recession and interest rates will recede in early 2024.

I’ll be keeping my eye on these developing stories in the coming months, as they not only impact the direction of mortgage rates but they will also set the landscape for the 2024 election season. Buckle up! It should be a wild 12 months ahead. Thanks as always for watching, reading and tuning into my content. Have a great weekend!

Another graphical anomaly is foreshadowing a recession (& lower mortgage rates)

If you’ve been following me, then you’ve heard me harping all summer long on how the interest rate markets are out of whack. With each passing month, more signals pop up to remind us that we are not in normal economic times.

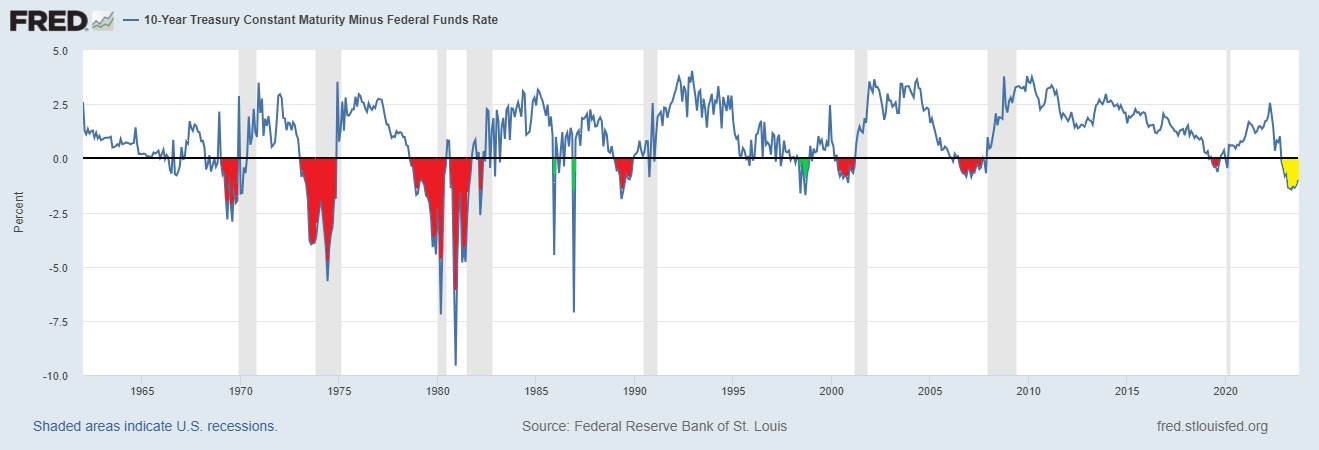

Earlier this month, The Fed held their Federal Funds Rate steady at 5.5%. This is the highest level since 2001, but how high it is RELATIVE TO other interest rates is what makes things so odd.

Below is a line showing the “spread” (simply known as the difference) between the rate on a 10-yr US Treasury Bond and the Federal Funds Rate. Typically, the 10-yr bond rate is higher than the Federal Funds Rate, making the spread a positive number. In fact, from 2002-2022, the spread has been negative for only 20 months during those 20 years.

But occasionally the Federal Funds Rate increases to unusually high levels, and this spread becomes a negative number. I’ve color-coded those extended negative territories in red, and you can see that a recession has shortly followed every time (illustrated by the gray vertical bands on the timeline). We have escaped a recession despite a negative spread a few times (shown in green), but those were for very brief periods before the spread quickly jumped back into positive terrirory.

Presently, we have witnessed a negative spread between the 10-yr bond rate and the Federal Funds Rate for nearly a year (yellow area on the chart). This is foreshadowing another upcoming recession, but the silver lining is that mortgage rates ALWAYS drop during recessionary times.

When will the recession hit? When will mortgage rates fall? I have some thoughts on that, but will save them for my next post. Thanks for reading, and stay tuned for more.

Our team has been making a ton of preparations to deliver loads of value in our upcoming seminar aimed at helping folks buy their first home.

As a REALTOR people always ask me, “Matt, when is the best time to buy a home?” The answer in real estate is always, “30 years ago!”

But a more helpful answer I can give is “right now!” Yes, as in Fall. Fall is for more than pumpkins, football and flannel. Statistically fall is also the best season for buyers to have the upper hand in the real estate market. Which is why we are hosting a FREE first-time home buying seminar at our Folsom office on Wednesday September 20th.

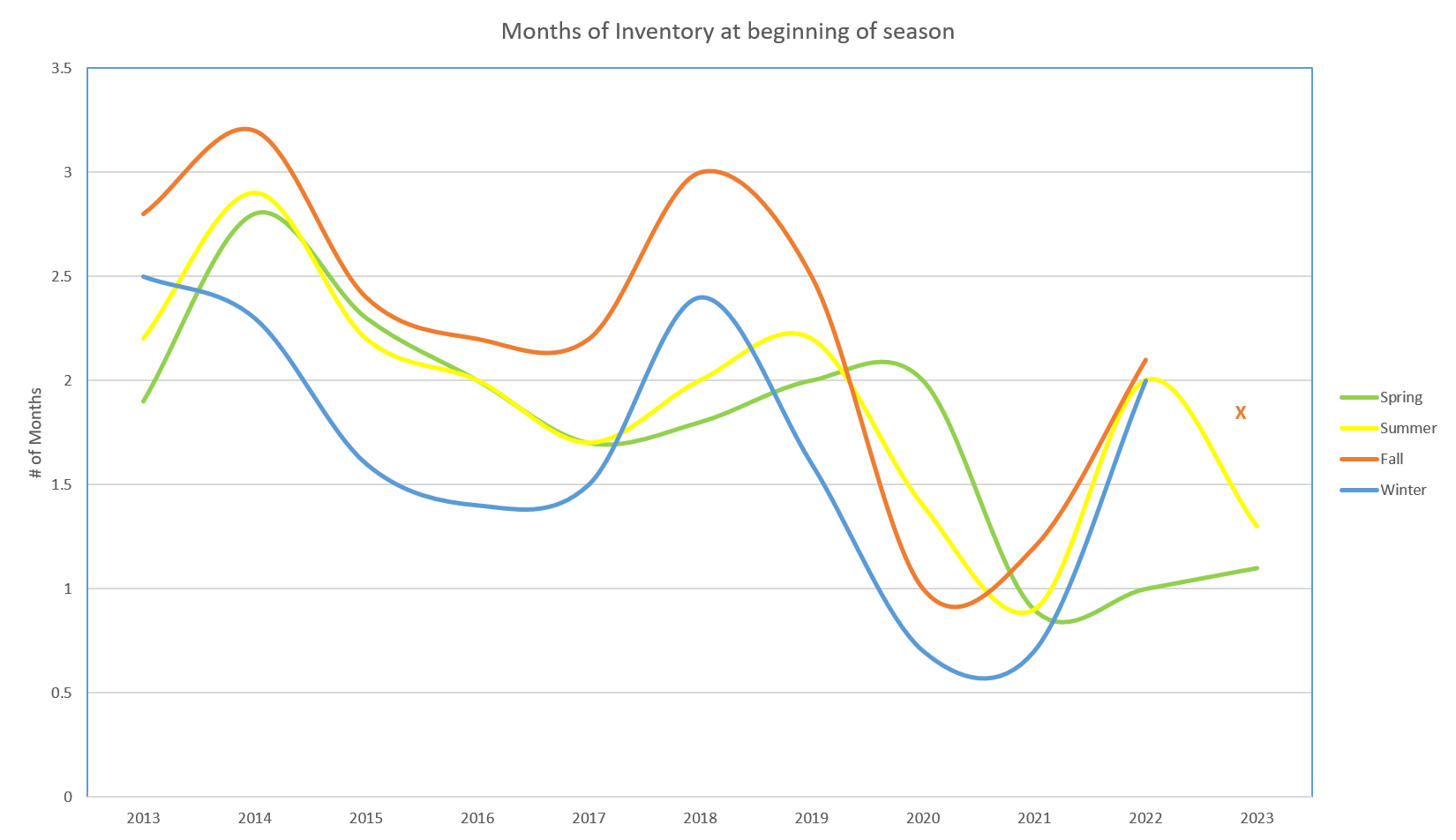

Below is a visual that shows how fall is the friendliest season for buyers. When comparing homes for sale (representing the number of sellers) to the homes that actually sold (representing the number of buyers), our industry calculates a metric known as “months of inventory.” In other words, how many sellers do we have compared to buyers. As a buyer, you want this number to be as high as possible, because it signifies more options for you and less competition against you. I plotted the last 10 years of Sacramento County home stats, and you can see how in every year (except 2020 when Covid turned everything on its head) the fall season (represented by the dark orange line) has been higher than all of the other seasons. Every. Single Year. And 2023 is shaping up to be the same; as of the time of this post the monthly of inventory stands at 1.7 months, higher than any other season so far this year.

Even if you’re not quite ready to buy right now but hope to buy a home in the future, you should still come and learn about down payment assistance programs, improving your credit score, and generally knowing what to expect when buying a home. You’ll also learn a bit about our firm and why we’re perfectly suited to help you both find and finance your first home.

There’s no cost or commitment to attend the seminar, but space is limited so register here before space fills up. Sign up, grab a pumpkin spice latte on the way and we’ll see you at our office on the eve of autumn & home buying season on Sept 20th!

This will be our final seminar in what has been a very successful Summer Seminar Series. We thank everyone for their attendance, enthusiasm and interest in these important topics we’ve brought to our clients and community this summer.

We have been hosting valuable seminars all summer long for our clients and community. Initially kicked off on the Summer Solstice back in June, our Summer Seminar Series concludes on September 20th with a seminar aimed at educating and empowering clients to purchase their first-home.

We’ve uncovered several statistical consistencies that show the upcoming Fall season is the best time of year to buy a home in the Sacramento area. This little known secret needs to be shared! We are going to be showing statistically why fall is the ideal home-buying season, explaining the preparation steps first-time home buyers should take, and so much more.

Be sure to share this post with someone in your life who has shown interest in buying a home. This in-person seminar is FREE to attend but space is limited. Click this link to register before space fills up.

More evidence lower mortgage rates should be on their way

At the beginning of summer, I wrote a fun Top Gun themed post about how inverted “yield curves” are an indicator that lower mortgage rates are on their way (click on the link above for a refresher).

As we now approach the end of summer, I’m doubling down on my projection based on another rare occurrence in the financial markets. Hear me out, check out the new charts, and let me know if you agree.

For those of us in the mortgage industry, its no secret that mortgage rates are closely correlated to the rates of US bonds. Here is a 40-year chart that shows these rates go up & down together.

But they don’t always go up & down by the SAME AMOUNTS. Investors of mortgages (blue line) always command a higher rate of return than a US Bond (red line). Why? Risk. Investors feel its more likely a homeowner will default on their mortgage debt than the US government will default on their debt (debatable, I know, but not for this post). Whenever an investor takes on more risk, they want more return.

Here is a chart that combines the blue and red lines from above into a simple visual showing the difference (or “spread”) between the two rates over time.

Over this same 40-yr period, the typical spread has been between 1.5%-2.0%, with a median of 1.67%. There have been a few instances when this margin has increased to over 2% during uncertain economic times (DotCom bubble, 9/11, Covid lockdowns). And when this spread increases to drastic levels over 2.5% it very quickly boomerangs back to levels below the orange line. But recently the spread has been hovering around 3%, nearly twice the historical norm and unprecedented during this time frame. Why??? Same answer…RISK! But a different kind of risk…prepayment risk.

Mortgage investments are a little different from government bonds in that most investors don’t expect a 30-yr mortgage to be a 30-yr investment. Many scenarios could cause a mortgage to be paid off ahead of schedule (sell the home, refinance, etc.). And the sooner a mortgage is paid off, more risk to the investor via stunted returns. The unprecedented, sustained level of the spread at nearly 3% is proof investors see high risk in buying mortgages in today’s market. Its clearly not due to foreclosure risk (those levels just hit 40+ year lows). Rather, its due to prepayment risk, as investors anticipate refinance opportunities for current borrowers when mortgage rates fall in the near future.

Lets recap:

The spread between mortgage rates and bond rates is crazy-high – when a metric is this out of whack, don’t expect it to stay that way for long

Investors see increased risk in mortgages due to refinances in the near future – the simple fact smart investors think new mortgages will have short shelf-lives is very telling

Either mortgage rates need to fall or US bond rates need to rise to bring the spread back in line with historical norms – Given that inflation is trending down and stock markets are already approaching all-time highs, it’s a safe bet bond rates won’t rise dramatically. Instead, expect mortgage rates to fall.

Dow Jones is near its all-time high

Inflation has returned to normal

The investors, and ultimately the financial markets, are telling us that mortgage rates will be falling. And likely they’ll be falling sooner than later. I will be keeping my eye on this market indicator, among others, as we track the mortgage and real estate markets. What will be important to forecast is what may happen when mortgage rates do finally fall. Do you have any guesses? You know I do!!! Stay tuned for more economic insight and projections. Thanks as always for reading.