Should you call a big bank to get the lowest rate? Nope!

Let’s get real about big banks. Some folks think that they need to go to a big bank like this one to get the best mortgage rate on their next home loan. When in actuality, nothing could be farther from the truth.

Chase Bank, the largest bank in America, has nearly 5,000 branches just like this one all across the country. In 2022 alone, they spent nearly $3 billion in advertising. So think about it…big banks with big expenses like this they need to earn big time interest on the loans that they issue in order to make a profit.

Last month as an example, I had a longtime acquaintance of mine reach out to me because he was in contract by a new house. He’s a big time depositor with Chase Bank so he reached out and got a home loan quote from them thinking that they would give him a smoking deal. Well, I was actually able to find a lender of mine that offered him an interest rate nearly half a percent lower than Chase’s rate saving hundreds of dollars every month on his mortgage payment.

So here’s the deal…as a mortgage broker over the last 20 years I don’t work with big retail banks that spend billions on advertising and rent. Instead I work with reputable wholesale lenders that have much lower overhead expenses and as a result they and I can offer you better rates.

Lets Get Real! Buying a Brand New Home can seem like the easy option in today’s real estate market. Picking your finishes and having tons of incentives thrown at you by a big builder sounds like quite the treat!

But that’s not what my latest client experienced. He called me last month really anxious because he had lost trust in the nationwide company building his new home. The worst of it was the in-house lender that was supposed to be giving him a great deal in fact wasn’t and clearly were inept at doing their job.

I was able to offer him an interest rate comparable to the builder’s advertised “unbeatable” offer, and more importantly ease my client’s nerves by having someone they trust involved in the process. They are set to close today and move in just in time for the holidays.

Here’s the take-away…even when buying a new home you still need your own real estate and mortgage advocates. Remember, the sales office is employed by the builder, so who do you think they’re looking out for first. I’ll give you a hint…its not you! And these in-house mortgage companies created by the builders are operating as loss leaders to get buyers in the door, which means they are probably not compensating their mortgage consultants very well, which probably means you’re not working with the sharpest knives in the mortgage drawer.

So, if you are thinking of buying a brand new home in the coming year, hit me up before even heading out to their model homes. We’ll discuss what you need to watch out for, and I’ll explain to you why having me involved in the process as either your REALTOR, mortgage broker or both is a huge benefit for you, and how you can have my representation services when buying a new home.

Over the past 15 years, I’ve provided an annual forecast of the mortgage and real estate markets. Generally, I speak to three main characteristics: housing supply, buyer demand, and interest rates.

This year, it’s all about the rates. If 30-yr mortgage rates remain at 7% or higher, housing supply and buyer demand will remain anemic. If they fall below 6%, we will see a flood of both buyers and sellers enter the market. Much of 2023 & 2024 saw rates largely stay within the 6-7% range, which led to generational-low transaction count and record-low affordability levels.

As such, it makes sense to focus my forecast on where interest rates may be heading in 2025.

Who Controls Interest Rates?

Many people are led to believe mortgage rates are controlled by select individuals, such as bank CEOs, The Federal Reserve Board (affectionately known as “The Fed”), or the sitting president (not sure what his affectionate nickname is at the moment). This is not correct!

Mortgage rates are actually controlled by the buyers and sellers of mortgage backed securities. In plainer words, mortgage rates move by investors trading mortgages. There is no man behind the curtain; no key players puppeteering rates, nor a president successfully demanding interest rates “to drop immediately“.

Instead, rates move based on risk & opportunity cost for these free-market investors. Let’s talk briefly about each of these factors.

First off, the biggest risk factor for a mortgage trader is inflation. Inflation eats away at the value of money, so when inflation increases traders don’t want to buy ultra-low rate mortgages. If they buy a mortgage bond with a 3% fixed rate, but inflation is at 4% they are actually losing money.

And opportunity cost is simply a question of can a trader buy an alternative investment with a higher rate of return & lower risk. So, no smart trader would buy a 3% mortgage when there are risk-free money market accounts offering 4% savings rates.

Below are the issues mortgage traders will be focused on in determining how much in mortgages they want to buy and at what interest rates.

Factors in 2025 that will push rates DOWN

Slowing Economy – Many sectors of our global economy have slowed down in recent quarters. Many factors could have contributed to this (political uncertainty, rising cost of goods/services, ), but generally interest rates fall during sluggish economic times. The primary driver of recent Gross Domestic Product (GDP) growth was personal consumption, but I believe personal consumption will slow in 2025 as households are forced to tighten their financial belts. Credit card balances are at record highs and continue to climb (check out my prior post about the alarming levels of household debt).

Lower Inflation – Rising prices on everything took a toll on most of the world in 2022-2023, but things are starting to ease. Inflation rates are now slightly over the historical trend and The Fed’s preferred level of inflation. Don’t expect prices of things to fall, but if they hold at near-constant levels then mortgage rates should decline.

Higher Unemployment – If fewer people are working, it is a sign of a weakening economy. While statistics continue to show 100-200K new jobs being created every month, this could change dramatically in the coming months. The largest employer in the US (the federal government itself) is mandating most employees to return to the office for work and looking to significantly scale back the total number of government employees. This could drastically change the employment picture, and push the unemployment rate up.

Factors in 2025 that will push rates UP

Long-term Tariffs – President Trump is using Executive Orders to impose or threaten tariffs on certain countries and certain products. Tariffs are essentially an added tax on goods that are made in a foreign country. Some people think this added cost will be absorbed by the foreign company who is importing the goods, but this is rarely the case with tariffs. The tariff is typically added to the cost of the item, meaning the end consumer (Americans) will incur these tariff expenses. If tariffs become more of an entrenched part of Trump’s foreign policy rather than a short-term negotiating tactic, it will drive up inflation and interest rates with it.

Smaller Labor Force – Between deportations and baby boomers retiring, the number of available workers could decrease. With fewer workers, employers will need to increase wages to entice people to the workforce. This will fuel the flames of inflation (as it did when we came out of the deepest economic trenches of the pandemic) and push interest rates up higher still.

Growing Government Debt – Our country is in debt more than ever before. Presently, we carry over $30 TRILLION in debt, which is over 120% of our Annual GDP. That percentage is similar to levels seen at the end of World War II. It made sense we were in debt up to our eyeballs after fighting a World War for 4 years, but this is the first time we’ve been at these levels during peacetime! Our government debt is sold to investors via Treasury bonds, and the more we go into debt the more we have to entice them to keep buying our bonds. This enticement is in the form of higher rates of interest earned by the investor (and paid by the borrower). If rates of gov’t bonds increase, then mortgage rates will follow suit as well.

What Will Win The Tug-of-War?

2025 will see these pressures pull against one another, and neither will be a clear-cut winner. I do believe the downward pressures will slightly win out, as some of the upward pressures (tariffs in particular) also tend to slow down an economy, which should lead to lower rates. Overall, if you start hearing the R-word (“recession”) thrown around in 2025, expect 30-year rates to finally dip below 6% by the end of this year.

If mortgage rates do considerably improve, there will be more real estate transactions but not necessarily higher home values. It is expected more homes will come up for sale (both new construction and resale homes), which will keep home values somewhat in check.

If mortgage rates end up increasing above 7%, then we could see home values fall. With affordability already out of reach for so many potential home buyers, worsening conditions will further reduce the already anemic levels of demand currently seen.

Do you have thoughts or insights to share about your local real estate market? Leave them in the comments section below.

Zillow operates as an advertising platform rather than a public information service. Higher search rankings for houses or agents do not imply quality; they reflect the amount spent on advertising. Users should be wary, as top results may simply be influenced by financial investment, much like Google’s advertising model.

Let’s Get Real about Loan Assumptions. With current mortgage rates holding steady at their highest levels in decades, some believe a way to afford their next home purchase is to assume a seller’s existing loan at a much lower interest rate. Sounds like a great life hack, right??!! Why take out a new mortgage at 7% or more when you can assume an old one at 3% or less? While it is true that some loans are assumable, the odds of one being available on a home that you actually like and end up buying are next to zero.

I helped a recent client locate a home in Fair Oaks that was perfect for them. The seller was a veteran; my buyer was a veteran. VA loans are one of the few types of loans out there that are assumable; seemed like a match made in heaven!

But here’s the unfortunate reality…the loan assumption application process is cumbersome and takes time; often 1-2 months. This particular seller wanted a clean, fast sale, so even though the listing promoted the assumable nature of the mortgage, the seller ultimately selected a buyer who could purchase the home without assuming the existing VA loan.

Very few listings will have an assumable loan. And those that do will likely be very popular, and the seller may not be inclined to go through the assumable application process. Sure, I can help you filter home searches based on assumable loans (there’s 14 for sale in all of Sacramento County at the moment & 21 sales in all of 2024), but I wouldn’t recommend hanging all of your homeownership hopes on an assumable loan.

A few short weeks ago, nearly everyone (including me!) was anticipating mortgage rates to move lower. The media hyped up the forecasts. The Fed fanned the flames of these forecasts. I provided analysis to support the forecasts. But the financial markets often have a way of humbling bold predictors.

In early September, 30-yr fixed mortgage rates were hovering just over 6% and flirting to drop into the 5s. Since then, however, rates have aggressively climbed and are now threatening to return to the 7%+ range. DOH!!! It turns out we all were dead wrong.

I have several clients who would have benefitted from a refinance in September. Those lower rates could have saved them hundreds every month, and the closing costs were reasonably low. But many took the gamble of waiting to see if rates would fall further. Their decision to not take “the bird in the hand” has left them wondering how long it may take for rates to settle back down.

That’s why we shouldn’t rely on crystal ball forecasts from anyone (including me!!!) to make decisions. My recent post titled “When Should You Refinance” reminded that we should let numbers decide for us. While I often provide analysis and predictions about the mortgage and real estate markets, I share with clients that timing the market can be a fool’s errand. Do any long-time followers remember this 2016 video post that spoke to market timing?

A refinance transaction is when I see the most clients attempt to time the market, and it’s the transaction that is hardest to pull it off successfully. I advise clients all of the time that timing a refi is just like gambling. There is more emotion than logic at play, and our feelings of wanting/needing a lower interest rate cloud our judgment.

In short, don’t listen to people or their interest rate forecasts. If you have a higher mortgage rate and would like to refinance, follow these three initial steps:

Determine how much lower you’d like your monthly payment to be. Most folks like to see at least $100/month in savings.

Multiply your desired monthly savings amount by 12. In most cases, this total should be your maximum amount you should pay for refinance closing costs.

Work with me to set a target rate that achieves both your monthly savings amount and closing costs limit AND STICK TO THE TARGET! I will monitor & track mortgage rates constantly and advise you when/if we hit your target.

Mortgage rates should eventually settle back down. Take this opportunity to get a plan prepared to act decisively when the next refinance opportunity presents itself.

We’re overjoyed to announce that Style Magazine recently recognized us as the #1 Real Estate Team and #3 Mortgage Broker in the Folsom/El Dorado Hills area! This dual distinction is a testament to our team’s dedication to delivering exceptional service and expertise in both real estate and financing.

A quick Zillow search shows over 4,000 real estate agents serving the Folsom area. Moreover, hardly any of these agents also offer financing, so earning awards in both categories is truly humbling. We’re grateful for the trust our clients have placed in us, and we’re thrilled that our unique, one-stop-shop approach resonates with our community.

We extend our heartfelt thanks to Style Magazine for this recognition and to our valued clients for their votes. Your support means the world to us!

Discover how our comprehensive real estate and mortgage services can elevate your next transaction. Explore my blog & website to learn more about our team and our award-winning approach to real estate.

Here are the factors to consider if you have a rate over 6%

Clients often ask me about “timing the market.” In other words, is there a way to get the best price or lowest rate based on WHEN you buy/sell/refinance? Last year I researched historical data of the past decade and posted about the best times of year to buy and sell homes in Sacramento. It revealed seasonal trends that show Winter (not Summer!) is the best season for sellers and Fall (right now!) is best season for buyers. Even Realtor.com supports my research in their own recent report that claims THIS WEEK (September 29-October 5) will be the best week this year to buy a home!

But how about timing a refinance? Is there a way to perfectly time the financial markets to assure you get the lowest possible mortgage rate on a refi? Let’s dive in and discuss!

As you may know, mortgage rates move every day. Much like stock prices, their daily gyrations are unpredictable even though many market experts spend their lives studying and predicting them. But surely there must be a way to know if mortgage rates will go up or down in the near future, right???

WRONG!!! We only need to look back a couple of weeks for clear proof of the erratic nature of mortgage rates. On September 18th, The Federal Reserve officially lowered the Federal Funds Rate by ½%. Many expected mortgage rates to follow suit, but surprisingly mortgage rates actually increased slightly upon The Fed’s actions.

Mortgage rate changes do not have seasonal trends the same way as the real estate market. To prove this, I studied data of 30-yr mortgage rates from the past 40 years, and found that mortgage rates don’t drop more frequently in one time of year over another. I recorded all of the months where mortgage rates fell, and noticed these tallies were evenly spread out throughout the year:

Season

# of Months w/ rate drops (since 1984)

Spring

73

Summer

52

Fall

76

Winter

77

As you can see, there is no season that significantly stands out above another. In fact, Spring, Fall and Winter had nearly the identical number of months that experienced rate decreases.

As an easy visual comparison between the real estate and mortgage markets, look at the rhythmic, predictable nature of the chart on the left showing home sales over the past 10 years (generally peaks in 2nd quarter; bottoms in 4th quarter) to the chart on the right showing 30-yr mortgage rates over the same time period (no pattern whatsoever).

Real Estate Sales look like a heartbeatMortgage Rates look like a seismograph!

If seasons are not an indicator, then perhaps significant events could be a tell-tale sign for mortgage rate movements…presidential elections, perhaps? Many people believe major elections create uncertainty in the financial markets, and generally mortgage rates fall in times of uncertainty. As a result, I’ve had some clients who could benefit from a refinance today gamble their guaranteed savings of today by holding off on a refinance decision until after this year’s upcoming election. Risky move, especially given the history of what mortgage rates do (or don’t do!!!) in election years.

I looked back at mortgage rates since 1980 and tracked the direction of rates in the months leading up to November. I found that in these 11 presidential cycles, 5 of them experienced rate increases while 6 saw decreases; a mixed bag with no clear trend. Most of these periods saw modest changes, with the average rate change being less than .5% over the 10-month pre-election intervals.

If the sun and moon and stars and elections can’t help us predict interest rates, then what should we look to instead??? Here’s my honest advice…ignore all of the “signs!”

Put away the tarot cards and pick up a calculator! When deciding when or if to refinance, stick to these simple factors:

What will today’s interest rate save me?

What will today’s interest rate cost me?

How long do I plan to have this loan?

Generally speaking, most of my current clients are choosing to refinance if they can recoup the closing costs within 12 months of their monthly savings amount. For example, if a proposed refinance costs $3,000, then it would make sense in most cases to do so if you can save $250/month or more. Doing so is allowing them to save money now, but keep the opportunity to refinance again if rates continue to fall in the future.

While these are straightforward calculations, the pros & cons of a refinance can be nuanced and best talked through with a trusted professional. As mortgage rates have fallen in recent months, aggressive marketing campaigns aimed at pressuring homeowners to refinance have increased dramatically. Don’t let an inexperienced sales call center guide you through an important financial decision; reach out to me to discuss your options.

Many believe mortgage rates are set to drop this week because of a highly anticipated Federal Reserve Board meeting that begins tomorrow. THIS IS WRONG! Mortgage rates are indeed poised to fall, but not because of The Fed meeting. Let me explain…

Last summer I wrote a similarly titled post about a rare phenomenon in the financial markets known as a yield-curve inversion. You can go back and read it (especially if you’re a Top Gun fan), or here are the brief Cliffs Notes…

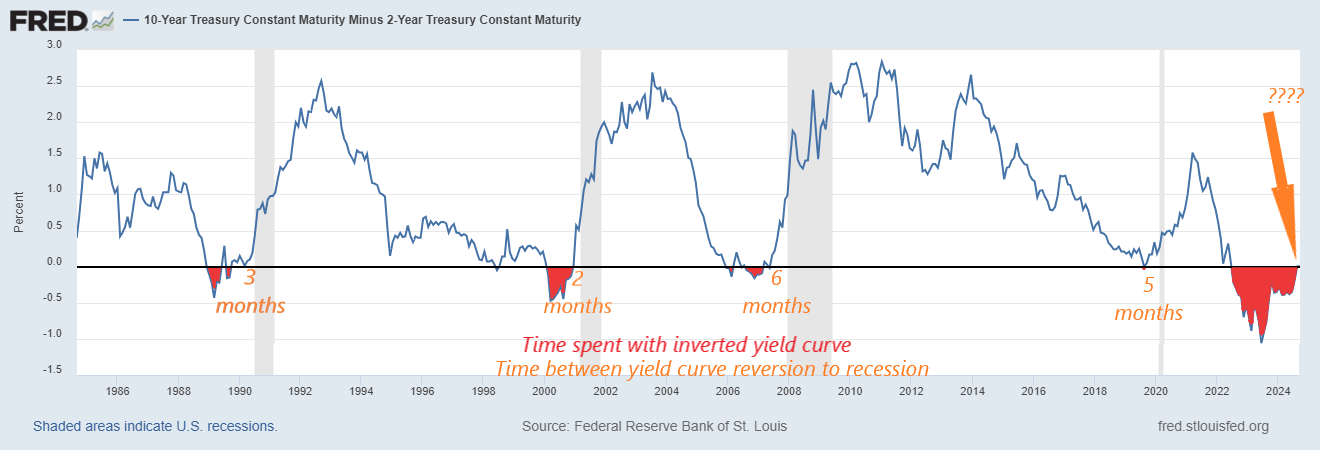

A yield curve inversion occurs when rates on short-term bonds are higher than long-term bonds. An inversion has only occurred 4 times in the last 40 years, and an economic recession has shortly followed each and every time.

Well, I’m here to update you on the yield curve and clarify the timing of the recessions that typically follow.

This month marks the first time in over two years where the yield curve is no longer inverted. It’s the longest continuous inversion period in modern economic times (sections colored in red on chart), and many feel it’s return to positive territory is long over-due.

But, this does not mean we are out of the recession woods. In fact, it’s typically a sign that economic troubles are just about to begin. A yield curve reversion to normalcy has preceded every recession of the past 40 years by just a few short months (2-6 months). If history repeats itself, then its only a matter of when we’ll be in a recession…possibly as early as later this year!

Some argue that we are already in one. Influential & entertaining economist Elliot Eisenberg finds that 9 of the 20 most reliable recession indicators have already been triggered. Historically, when at least 6 of these indicators are flashing red, a recession was already occurring or was about to.

This is not meant to be a doom & gloom post. In fact, quite the opposite!!! The real estate and mortgage markets have been in a funk for the past 2 years, largely due to higher interest rates. The silver lining to an economic recession is it will likely lead to significantly lower mortgage rates. Lower rates will help struggling homeowners consolidate debt more affordably, aspiring home buyers to break into the market, and hesitant home sellers feel less locked-in to their current low-rate mortgage.

All in all, a mild recession and lower mortgage rates could be healthy for our sputtering real estate market. Time will tell if and when lower rates are coming, but if you’ve been holding off on making a big real estate decision due to high interest rates, then you should begin reconsidering your options now. Give me a call to discuss where rates are at, where they may be heading, and what they need to get to in order to help you make a confident decision in your real estate affairs.

A recent research study concluded that consumers get the best loan terms when working with a mortgage broker! In short, the average interest rate AND origination points paid through a mortgage broker were both lower than when working with a retail lender (think big banks). The savings were even larger on government loans!

Don’t just take my word for it; check out the research findings here and be reminded of why it’s important for you and your loved ones to work with mortgage brokers like The Blue Waters Group!