Let’s Get Real about California’s new loan program coined Dream For All. The Blue Waters Group has this shared appreciation 2nd mortgage available to eligible applicants, but is it really a Dream “For All?”

It truly is a great loan program for those who qualify, as it will allow folks to buy with no money down, avoid PMI, and keep their monthly payment at a reasonable level, but

The program is, unfortunately, underfunded. The state legislature recently allocated $300,000,000 in funding for CalHFA’s Dream For All loans, which will likely only reach approximately 2,000 California applicants. To put that in perspective…our state had over 250,000 transactions in January alone. So Dream For All loans will impact less than 1% of transactions.

This program is getting a lot of hype and I am happy to help you apply for it before the application window closes in the middle of March. Keep in mind, however, it will not end up being a Dream For All, but rather For a Very Lucky Few.

With that said, it’s a great program if you qualify and are fortunate to have your name pulled in the lottery system. Reach out to me and I can help you navigate the application process and give you more details about CalHFA’s Dream For All loan program.

After several years of sharp increases and unpredictable swings, mortgage rates have finally entered a period of relative stability. While rates remain higher than the historic lows of 2020–2021, the consistency we’re seeing in recent months is creating something the market has been missing: confidence.

30-yr chart from Mortgage News Daily

So what does this mean if you’re thinking about buying or selling?

Stability Brings Predictability

When mortgage rates move dramatically, buyers tend to pause. Rapid changes create uncertainty about monthly payments, purchasing power, and timing.

Stable rates, even if they’re not “low,” allow buyers to:

Calculate payments with confidence

Plan financially without fear of sudden spikes

Move forward without constantly trying to “time the market”

In other words, stability reduces hesitation.

It Could Always Be Worse

Given the incredible volatility in financial markets over the past year, we should be thanking our lucky stars that rates are as low as they are. Stubborn inflation, low unemployment rates, stock market rallies, tariff wars, record government debt levels, international conflicts, and domestic unrest have consumed headlines over the past year. These are all factors that tend to push rates higher. And yet, mortgage rates have fallen 1% during that time. Phew!

Buyers Are Adjusting

The initial shock of rising rates initially experienced in 2022 has worn off. Today’s buyers are adjusting expectations and focusing on:

Long-term value

Negotiation opportunities

Seller concessions

Sellers Benefit from Serious Buyers

Stable rates also filter the market. The buyers actively shopping right now are motivated and realistic. They’ve done the math. They understand today’s financing environment.

For sellers, that means:

Fewer “just looking” showings

More qualified buyers

Stronger negotiations

Less last-minute fallout due to rate swings

Well-priced homes are still moving.

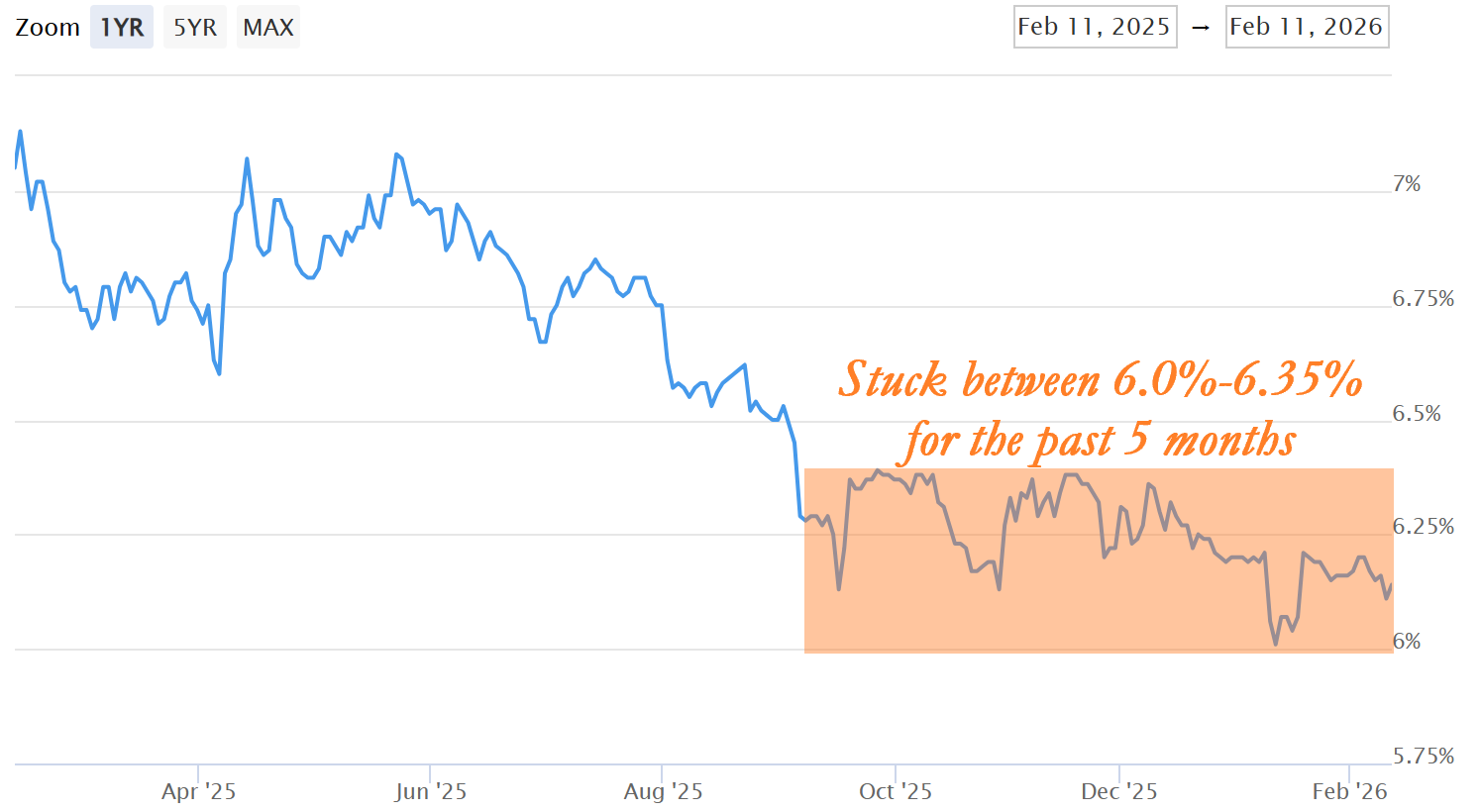

Return to a More Normal Market

For the past 5 months, rates have stayed within a .3% range; the lowest level of volatility seen since 2021. When rates are flat like this, buyers & sellers both begin to accept these rates as the new normal and make more confident decisions.

Bottom Line

Stable mortgage rates may not grab headlines the way dramatic hikes or cuts do, but they bring something even more important: confidence and clarity.

It’s that time of year where one day feels like summer and the next winter. Last week I put away my outdoor furniture, only to want to haul it out just a few days later to enjoy the warm sunshine! And today the forecast was for over an inch of rain and it’s looking like we won’t even get half that. It’s tough to plan with such wild weather swings!

The real estate market is similar at the moment. After an encouraging September where home sales surprisingly increased year-over-year in most parts of the state, October showed disappointing figures. With such inconsistent trends, identifying the vibe of the market is harder than ever. The government shutdown, high cost of living, and unpredictable mortgage rates are all impacting the real estate market in unpredictable ways.

You can read the signs

and still get it wrong!

I have a number of clients hoping to sell their homes in the coming months, and many of them are trying to time the market. They ask me questions like,

“Should I list for sale now before the holidays?”

“Should I wait till Spring?”

“How much more will my home be worth in 2026?”

Just ask me if it’s going to rain on Christmas while you’re at it! In all honesty, timing the market is a lot like timing the weather. You can read the signs, but ultimately its impossible to pull off every time. Here’s a throwback video I shot discussing this analogy.

Even though I’m an expert and live & breath market statistics and trends, I can’t predict the real estate future with any certainty. That’s not what you should expect of me or any real estate professional. What you should expect is help identifying what is most important in your next real estate transaction and navigating through it without losing sight of your priorities. Sellers often get caught up in timing the market that they forget why they are selling in the first place.

I have a client who lives in a home that no longer suits her and the property is bleeding her money in repairs. There are 2 homes that sit on 10 acres and require a lot of upkeep, so this widower recognizes she needs to live in a simpler, low-maintenance home. That is the priority; to change her lifestyle that will improve her health and finances.

But sadly, the quest of maximizing her sales price based on market timing has taken over. And during this quest, she has changed her mind several times, questioned herself, and ultimately is shackled in indecision. All the while, the property expenses are piling up and she loses sleep worrying about what to do. She keeps asking herself “when,” while the most important question she needs to ask herself is “WHY.” Why am I selling my home?

Does this sound familiar to anyone you know? Perhaps your own situation? When toiling over an upcoming home sale, ask me these questions instead:

“What is my home worth right now?”

“Where should I put my focus on improving my home for a sale?”

“Who can help me make this process as easy as possible?”

In short, control your controllables, and most importantly…FIND YOUR WHY. Why are you selling your home? Allow me to help you never lose sight of that.

For the second year in a row, The Blue Waters Group earned the Top Spot as the #1 Best Real Estate Team and inched up to #2 as the Best Mortgage Broker in the Folsom/El Dorado Hills region of Style Magazine’s Readers’ Choice Awards!

These awards are based entirely on votes that come from community members. THANK YOU to our many clients who recognized us with top marks in both our real estate and mortgage services.

Check us out in the October issue of Style Magazine; on newsstands now!

Our track record of earning these distinctive awards as both a Mortgage Broker and Real Estate Team show we are truly a unique business in our region. From helping you find AND finance, buy AND sell, refinance AND invest, The Blue Waters Group is capable of handling ALL of your real estate needs.

I’m sure you’ve heard the news…mortgage rates have finally been falling! But if you’re sitting on a high mortgage rate should you hold off on a refinance until after the upcoming Fed press conference?

Many people expect The Federal Reserve to lower the federal funds rate 1/4-1/2% on September 17th. But what most people misunderstand is this has no bearing on when or even if mortgage rates drop. Mortgage rates have already fallen nearly ½% in the past 30 days due to the same market conditions that are prompting The Fed to cut their rate next week. Mortgage rates don’t wait for Fed policy; mortgage rates change in real time as market conditions change.

Here’s my advice…if your mortgage rate is currently at 7% or above and you have good credit and home equity, look into refinancing now. Don’t get greedy and hope rates get even better next week. It’s worth pointing out that the last time The Fed lowered their rate, mortgage rates actually increased. As the old adage goes, better to take the bird in the hand, instead of two in the bush.

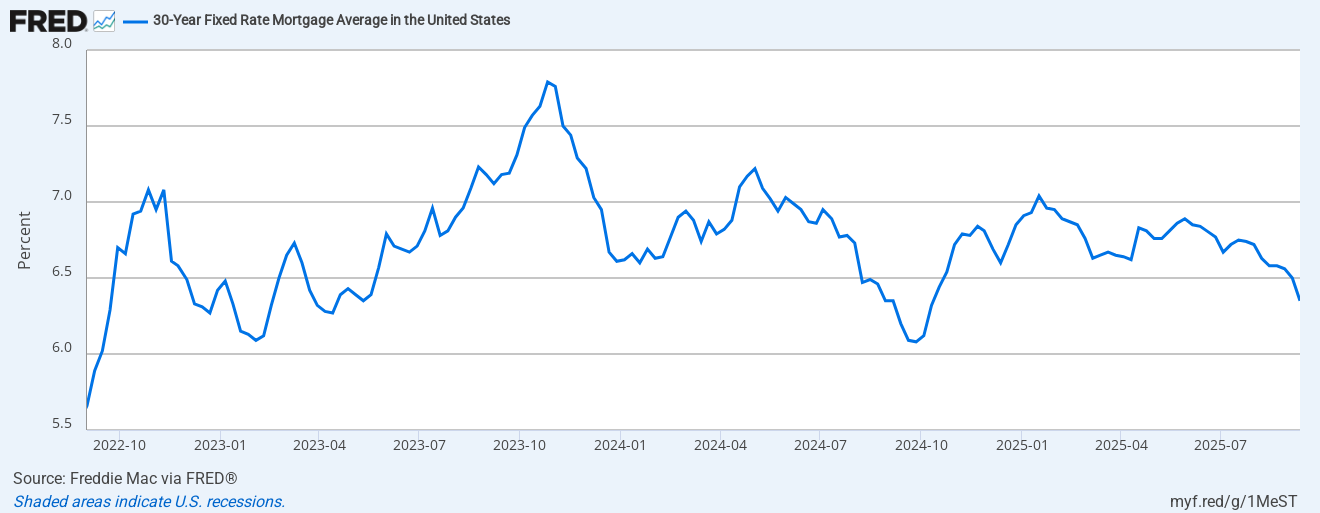

As the chart below illustrates, mortgage rates have not dipped below 6% in the past 3 years. And each time they approach that barrier, they bounce HARD in the other direction, rising 1.0-1.5% in the following months. We are testing that 6.0% barrier again. Will it break through this time? Or get rejected for the third time in three years?

But, if your mortgage rate is already in the 6s and you’re not interested in shortening your term to a 15 yr loan, then “roll the dice.” Sit tight and see if rates fall further. I wouldn’t count on it happening right away, but there’s always that small chance lower rates are on their way.

I’ll be working this weekend and can even lock your refinance rate during after-market hours. Hit me up if you want to explore your refinance options with an experienced & local mortgage broker before the high volatility of next week’s Fed meeting impacts the financial markets.

We’re thrilled to share that we have been nominated again as Best Mortgage Broker and Best Real Estate Team in Style Magazine’s 2025 Best of the Best Readers’ Choice Awards!

You may recall we earned awards in both categories in 2024, and we are looking to repeat these high honors. As a small (but mighty!) team, we pour our hearts into helping you buy, sell, and finance your home—offering top-notch service and interest rates that make you and your wallet smile. It’s our passion, and it means the world to be recognized for what we love to do.

Now we need a quick favor that’ll only take a couple of minutes—but gives you lifetime bragging rights for helping us achieve the highest honor: 1st place in both categories!

👉 To cast a valid vote, you’ll need to vote in at least 10 categories.

To make it easy, we’ve put together a cheat sheet with other incredible local businesses we admire and think are vote-worthy, too. But of course, feel free to choose your own favorites!

Your support truly means everything to us. Thank you for being such an important part of our journey—we couldn’t do this without you! 🏡💛

The world’s financial markets are currently in chaos as a global tariff trade war escalates. For the first time ever, the Dow Jones stock market dropped more than 1500 points two days in a row. The S&P 500 stock market is down more than 20% in recent weeks, a textbook “bear-market” collapse.

Fear, uncertainty, and panic are beginning to set in. Typically, these types of market sentiments lead to lower rates.

Dow Jones stock market free falling!

But contrary to recent sensational headlines and advertisements, mortgage rates have not had a huge slide…yet. Last week, 30-yr rates fell .15% to their lowest levels thus far in 2025. That has spurred a tremendous amount of refinance marketing activity amongst mortgage companies. But the reality is most folks with rates under 7% still won’t realize much benefit from a refi.

Mortgage Rates are improving, but not as much as the media and advertisements may suggest

If things continue, however, there will be tremendous refinance opportunities for many homeowners. As always, I will keep a watch on the financial markets and reach out when I see realistic refinance opportunities for my clients.

If you are hoping to refinance to a lower rate, temper your excitement for now. Don’t fall for the premature hype being pushed by aggressive mortgage marketing companies. But, it would be a great time to begin the application process with me as we await rates to drop further.

Let’s Get Real about Marketing in the Real Estate Business. It’s common for professionals to automate their advertising by subscribing to marketing content that is created and published by a 3rd party.

But this style of marketing gives zero insight to your brand, skills or personality, and can often backfire when many of your competitors are copying & pasting the same generic marketing materials.

I make a point of creating all of my own marketing content. Call me old-fashioned and inefficient for doing so, but it also makes me genuine and authentic.

I am very excited to pass along a big announcement from two of my biggest competitors. Why?!? Let me explain.

Earlier this week, Rocket Mortgage, one of the largest mortgage companies in the country, spent nearly $2 BILLION to acquire Redfin, one of the biggest names in real estate. You may recall that Re/Max (the largest real estate brand in the world!) did something similar back in 2016 (I wrote about it then too).

They aim to create a “one-stop-shop” experience for clients so they can buy, sell, and finance homes from a single source. Hmmmm, why didn’t I think of that? 😉

The biggest brand names in real estate are joining forces and copying my one-stop-shop business model. Some may say this trend of big companies creating end-to-end consumer “ecosystems” is bad for my business. Should I be concerned about my market share?

Perhaps, but the overwhelming feeling I have is one of flattery. I’m absolutely flattered that the likes of Rocket Mortgage and Redfin, publicly-traded companies valued at BILLIONS of dollars, are trying to emulate us!

The Blue Waters Group has believed from our very beginnings that the customer benefits from competent and compassionate advisors who can offer both mortgage and real estate services. With Rocket Mortgage & Redfin literally spending billions of bucks, no longer is our business model the obscure alternative; it is the one that leading industry players are striving for. No longer is our platform one that I need to defend with blog posts titled Is What I Do Legal?; it is the one that’s copied by others.

We are still unique from these big company aspirations in that our associates are able to offer both mortgage and real estate services (all of us are licensed both as mortgage loan originators and real estate agents) while Rocket simply hopes to pair mortgage and real estate services more efficiently by providing them under the same corporate umbrella. Nevertheless, this week’s move by Rocket Mortgage & Redfin further validates the craft I’ve been honing for nearly my entire career.

Working as both a mortgage broker and REALTOR is not an easy task, but with a 22-year head start on these firms and others who are sure to follow suit, I’m confident The Blue Waters Group will continue to be imitated but never duplicated!