A recent research study concluded that consumers get the best loan terms when working with a mortgage broker! In short, the average interest rate AND origination points paid through a mortgage broker were both lower than when working with a retail lender (think big banks). The savings were even larger on government loans!

Don’t just take my word for it; check out the research findings here and be reminded of why it’s important for you and your loved ones to work with mortgage brokers like The Blue Waters Group!

Timbuk 3, a 1-hit wonder from the 80s, wrote “Future’s So Bright, I Gotta Wear Shades” and is often interpreted to mean there are exciting events ahead. For example, I couldn’t help but hum the song this past weekend as we helped move our daughter into her freshman dorm at college. She has her whole life in front of her; full of potential and promise. Her future indeed looks bright and we are so proud of her!

But, the band actually ironically intended the song lyrics to be a grim outlook of nuclear fallout fears during the height of the Cold War. The shades referenced were not a cool fashion statement, but rather to protect your eyes from a bright nuclear blast!

I study nuclear science

I love my classes,

I got a crazy teacher

He wears dark glasses.

*image from Universal’s Oppenheimer film

Where am I going with this??!! Well, the current economy is at a crossroads and up for varying interpretations as well. After three years of rampant inflation, interest rates have begun falling. We are currently helping several folks refinance who purchased homes in 2023 at higher rates, and we expect to do much more of that in the coming months. You can say the future looks bright for those looking to refinance and save on their mortgage payment!

Mortgage rates have sharply declined in recent weeks to levels not seen in over a year!

On the other hand, interest rates are settling down largely due to growing signs of a slowing economy. Unemployment rates are rising, global stock markets are very volatile, and statistical patterns suggest a recession is right around the corner (see below). While the future looks bright for mortgage rates, a larger economic doom could also be on the horizon.

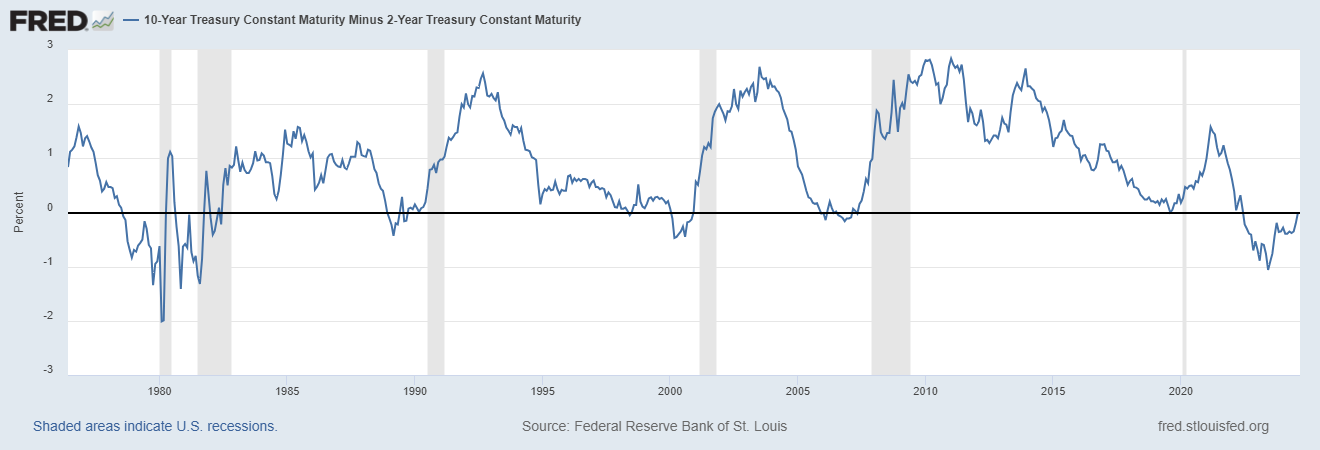

By many metrics, we are on the eve of a recession. This graph shows the rising unemployment rate compared to the levels of the year prior. When the blue line hits .5%, many consider we are in a recession (known as the Sahm Rule). In July, the reading was .53%!For the last 40 years, every time this blue line reverts back above the flat black line after falling into negative territory, a recession (areas indicated by the gray horizontal bands) has followed. As of August 30th, the line is finally out of negative territory after being negative for 25 months (the longest duration in my lifetime!). For more insight on this statistical relationship, read my Top Gun themed post from last summer.

If you have been waiting for a lower mortgage rate to either refinance or purchase a home, the future does indeed look bright for you. You should call us now to set a “target rate” that makes sense for you to pursue a refinance or home purchase. Let us help you look at the market through the right “shades” and keep an eye on factors that may push rates lower so you can best prepare for a refinance opportunity.

Future’s So Bright (for mortgage rates), Gotta Wear Shades!

On Wednesday, The Federal Reserve Board left their Federal Funds Rate unchanged. This was widely expected amongst financial markets, yet stock markets rallied and mortgage rates fell at once. What gives?

Simply put, markets change when the expectations of future events change. They don’t wait for the actual event to take place. To illustrate, here is a chart showing how The Federal Funds Rate (in red), has not changed in 12 months and yet mortgage rates (in blue) have been bouncing all over the place as market expectations have evolved over a myriad of variables (inflation, elections, economy, etc.).

This week was no exception; markets followed the words and largely dismissed the actions of The Fed. While the Federal Funds Rate was left alone, The Fed strongly suggested they see economic conditions that merit lowering the rate in future meetings later this year. Markets cheered these words, as mortgage rates had one of the best weeks in some time!

It can be hypocritical for parents to insist that their children “do as I say, not as I do.” In this case with the markets being the “kids” and The Fed being the “parents,” the market is dutifully following the words of The Fed by pushing mortgage rates down despite The Fed holding their rate steady. In fact, mortgage rates dropped to their lowest levels since April 2023, and will fall further if The Fed keeps true to their word in their next meeting. But, if The Fed reverses course like a hypocritical parent, then the markets (& mortgage rates specifically) will throw a fit and rise rapidly.

All in all, it has been a great week for mortgage rates. Let’s hope this rally continues!

A key inflation metric turns negative for the first time since the initial Covid-19 outbreaks

For the past few years, interest rates have remained at elevated levels due to high inflation. The words to describe the inflation have evolved over time; initially it was called transitory, and then persistent, stubborn, and sticky. Now inflation can be called negative.

Chart from YCharts.com

This week’s Consumer Price Index dropped to -.06% since last month, the first time it’s been negative since the darkest economic months shortly after the initial Covid-19 outbreaks and subsequent economic shutdowns. Moreover, it’s the first time since this battle with inflation began that the month-over-month reading has decreased for 3 consecutive months.

This news is significant for anyone who borrows money (or is planning to borrow money). To combat inflation, governments around the world have increased borrowing costs. The US Federal Reserve Board has consistently reminded markets that they will not lower rates until they are confident that they are on a path to return inflation to their annual target of 2%.

After Thursday’s inflation report, markets are optimistic that the battle against inflation is finally being won. As a result, mortgage rates are falling. For the past 3 months, 30-yr fixed mortgage rates have bounced between 7.0-7.5%. As of yesterday, they are decidedly below 7% for the first time since Easter.

Chart from MortgageNewsDaily.com

I remain cautiously optimistic that lower inflation readings like this week’s CPI report will become commonplace in the coming months. If that becomes the case, then mortgage rates should continue to fall.

If your credit card balances are creeping up on you, it may be time for a cash-out refinance

Total US household debt continues to climb even as borrowing costs rise with higher interest rates, particularly on credit cards. The total debt level for credit cards hit a record amount of $1 trillion…with a T!!! And it seems on pace to keep on climbing.

Many of us are facing harder times with the on-going economic slow down & lingering inflation. With credit card balances & their interest rates at all-time highs, it may be time to consider a cash-out refinance to consolidate high-rate loans.

Home values remain reasonably resilient & most homeowners have record levels of home equity. Even with elevated mortgage rates, it may be better to roll higher rate credit card debt into a new mortgage balance.

Has the economic slowdown forced you to borrow more against credit cards, cars, and education? Borrowing from your equity at a lower rate to pay off higher rate debt will lower your overall monthly payments and lower your interest costs over the long-run. I can help you determine the “blended rate” of your various debts, the effective interest rate you’re paying across all of your loans (including your mortgage). If your blended rate is over 7%, then its time to consider a cash-out refinance.

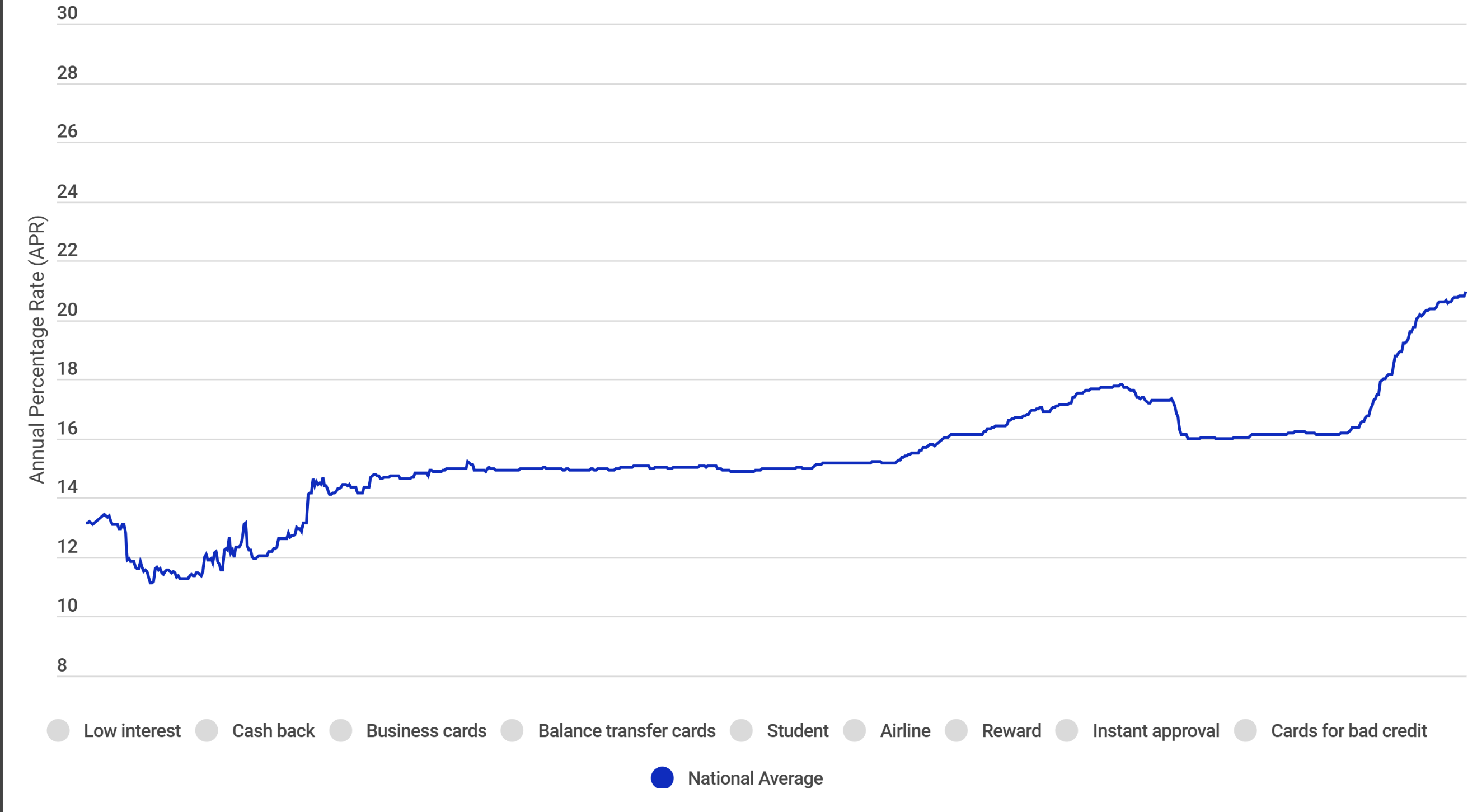

Consider the following graph…according to CreditCards.com the national average credit card interest rate is over 20%!. With The Fed suggesting they don’t plan to reduce the Federal Funds Rate any time soon, this will lead to high credit card rates for some time.

Let us help alleviate the financial stress of carrying high credit card balances at astronomically high interest rates by refinancing them into a lower fixed rate mortgage.

May seems to always be the most hectic month of the year. Graduations, picnics, school parties, sports, boating…commitments and fun keep us busy all month long, and I’m sure the same is true for you.

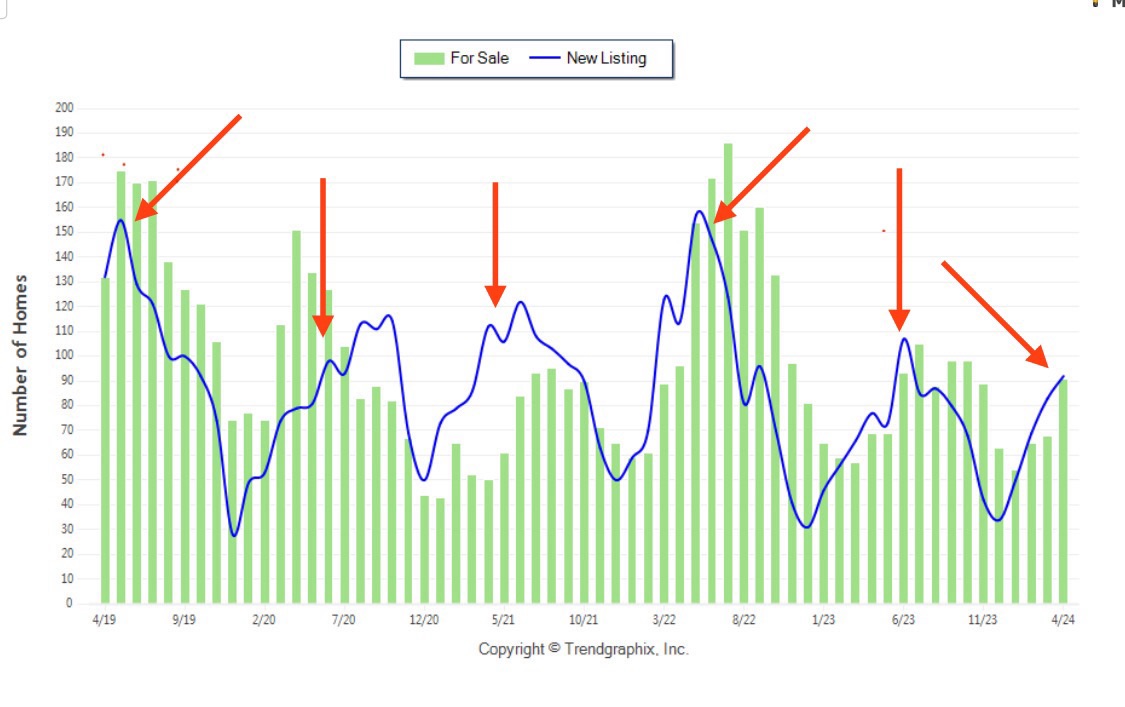

The real estate market has a way of hitting its full stride in May as well. For the last few years, May has signaled the time when many homeowners decide to put their homes on the market. This year appears to be similar as I’ve already listed two homes for sale in recent days. This is a good sign for the market at large since the single greatest issue we have in our market is too few homes for sale. Yes, that’s a bigger issue than high mortgage rates (although one could argue these issues are linked together)!

At the time of this writing, there are fewer than 100 single-family homes for sale in Folsom.

May is often when new listings hit their annual peak

This is an incredibly low amount, considering we are a town of over 80,000 people and 28,000 housing units. Over the last few years, beginning in May, we start to see this figure increase through the summer months, but since interest rates began rising two years ago we have seen the number of homes for sale in the summertime decrease dramatically.

What will this summer bring? Unfortunately, much of the same. Unless I get more calls from clients interested in selling their homes this summer, I expect the number of homes for sale to be similar to last summer. For current homeowners not looking to move, this is great news. For those looking to buy their first home, this is truly discouraging, at least for now.

I am anticipating mortgage rates to improve in the second half of the year, which will likely do two things: #1) more buyers will re-enter the market due to improved affordability; and #2) more “move-up” and relocating sellers will choose to put their home on the market as they feel less committed to remaining in their current home to hold on to an ultra-low mortgage rate. This increase in both demand and supply should keep prices level while increasing options for buyers.

Much like May’s relentless calendar, the real estate market keeps chugging right along despite challenging conditions. Either way…Bring. It. On.

Our team has become well-versed with the new California Dream For All Loan program and is ready to offer it to first-generation home buyer clients when the program is released next month. Let’s unpack a common example and see how this program functions.

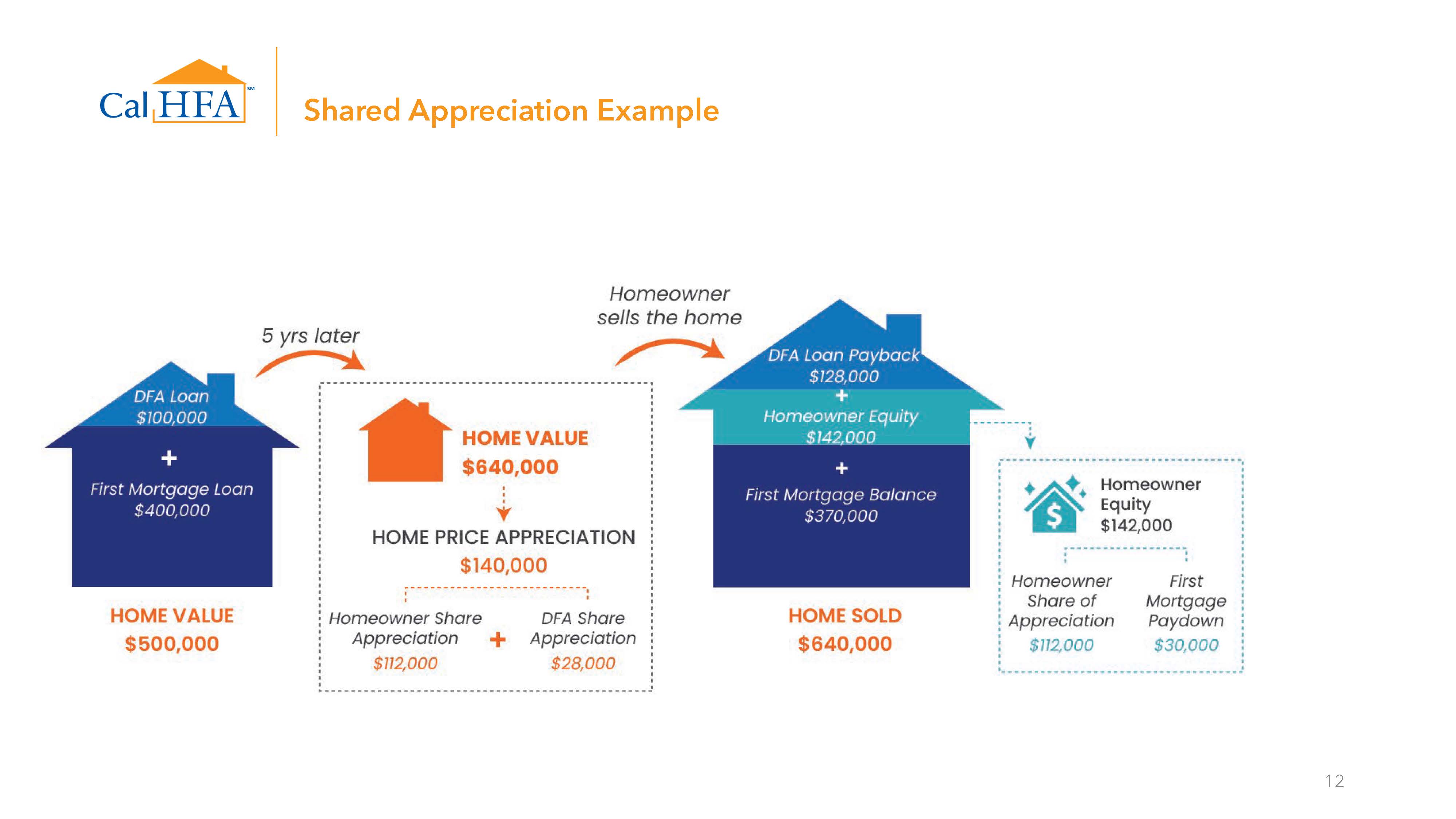

Assume someone buys a home for $500,000. They would obtain a traditional 30-year fixed loan at a fair market interest rate for 80% of the purchase price, making the loan $400,000. Now instead of making a $100,000 down payment, something most first-generation home buyers don’t have, they obtain a 2nd mortgage from the state of California for the needed $100,000. No monthly payments are required and no interest accrues on this $100,000 2nd mortgage. But it is not a grant; it is not free money. This 2nd mortgage is a Shared Appreciation Loan, meaning that when the home buyer goes to sell the property they have to pay back the loan in full AND share in the gained equity with the state of California.

Lets see how those numbers work. Lets assume this $500,000 home appreciates over the next few years and is now worth $600,000; it has appreciated by $100,000. Most folks utilizing this program will need to pay back 20% of that appreciation to the state, in this case $20,000 dollars. So when they sell the home, they will pay $120K to the Dream For All mortgage, the outstanding balance of the 1st mortgage that started at $400,000, leaving them with $110,000 in equity before selling costs.

So, in a nutshell, a borrower who put in nothing for a down payment ends up earning nearly $110,000 in realized equity. And to do so, they had to pay $20,000 in shared appreciation to borrow a $100,000 loan.

Here’s another example created by CalHFA worth taking in:

Like any loan program, there are qualifying restrictions and there are limited funds available so a lottery system is being implemented by the CA Housing Finance Agency to award approximately 2,000 folks to utilize the program. Contact my team and I for the full details on how first-GENERATION home buyers can take advantage of this new loan!

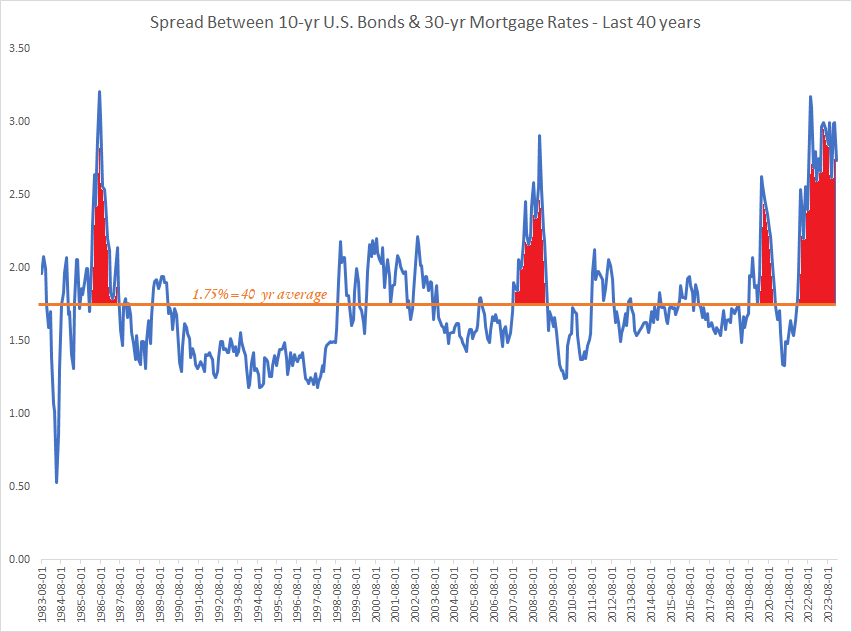

The difference between mortgage rates & U.S. treasury rates (aka-The Spread) is the story to watch in 2024

For the past 6 months I’ve been pointing out how many interest rate markets are out of whack. While technical in nature, these topics are SUPER IMPORTANT to watch if you are even remotely interested in the future direction of mortgage rates. Since most of my readers either own a home or hope to own one in the near future, this content is critical to cover and keep you informed.

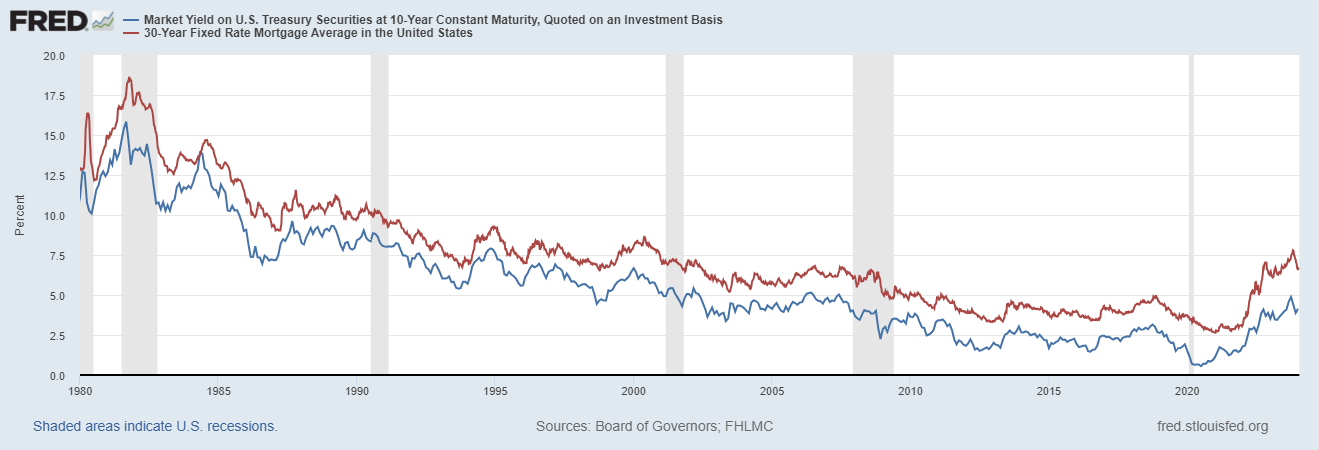

Typically, most interest rates trend in generally the same direction (up or down). Here is a chart showing how both mortgage rates and treasury rates have been in sync with one another over the years.

But these normal relationships have severed as of late. Mortgage rates have risen at a faster pace than treasury rates, and remained at these inflated levels for nearly two years. These oddities have occurred before in prior decades, but generally when things get out of whack they snap back in order fairly quickly. Presently, the difference, or “spread”, between rates on 10-yr treasury rates and 30-yr mortgage rates stands at 2.78%, over 1% higher than the 40-year average!

As you can see in the historical chart, there have been only two prior instances when this spread has flirted near 3%. In both cases, things returned fairly quickly back and even bottomed out well below the long-term average. This time around, however, the spread has lingered at nearly 3% for over a year and a half!!! I shaded in red the duration the spread lingered over the average of 1.75% to easily illustrate how odd the current episode looks.

What gives? My prior post on this topic explained the two distinctive risks investors face when purchasing mortgages versus treasury bonds (in short, foreclosure risk & pre-payment risk). Market experts are stumped as to why investors continue to see such high risks in mortgages. The Mortgage Bankers Association president forecasted just last week that they anticipate this spread to reduce as we proceed through 2024. Falling inflation & The Fed’s pivot on their approach to fighting inflation are the cited reasons why investors will see lower risk in mortgages, which will lower the spread and will ultimately lower mortgage rates.

The next test of this theory is coming up at the end of the month when The Fed meets next. At their last meeting on December 13th, we saw this spread drop severely as investor’s recalculated their perceived risks of holding mortgage bonds. Let’s hope January’s meeting has a similar result!

Let’s Get Real about BIG BANKS! They have big-time overhead expenses, so they have to earn big-time interest on their loans. For the best rates, skip the big banks use the services of a mortgage broker like me.

This is not about supporting local or shopping small. This is about getting the best deal possible on your next home loan!

Click on this link to read about how the rates I offer my clients tend to be nearly 1/4% lower than the average national mortgage rates!

If your credit card balances are creeping up on you, it may be time for a cash-out refinance

Total US household debt continues to climb even as borrowing costs rise with higher interest rates, particularly on credit cards. The total debt level recently hit a NEW record amount of $17.29 trillion…with a T!!!

$1.08 TRILLION is attributed to credit card debt! Many of us are facing harder times with the on-going economic slow down, lingering inflation, and the resumption of federal student loan repayments. With credit card balances & their interest rates at all-time highs, it may be time to consider a cash-out refinance to consolidate high-rate loans.

Home values remain reasonably resilient & most homeowners have record levels of home equity. Even with elevated mortgage rates, it may be better to roll higher rate credit card debt into a new mortgage balance.

Has the economic slowdown forced you to borrow more against credit cards, cars, and education? Borrowing from your equity at a low rate to pay off higher rate debt will lower your overall monthly payments and lower your interest costs over the long-run. I can help you determine the “blended rate” of your various debts, the effective interest rate you’re paying across all of your loans (including your mortgage). If your blended rate is over 7%, then its time to consider a cash-out refinance.

Consider the following graph…according to CreditCards.com the national average credit card interest rate is over 20%!. With The Fed suggesting they don’t plan to reduce the Federal Funds Rate any time soon, this will lead to high credit card rates for some time.

Let us help alleviate the financial stress of carrying high credit card balances at astronomically high interest rates by refinancing them into a lower fixed rate mortgage.